Public pension and other post-employment benefit (OPEB) plans face a common challenge: investing assets to meet long-dated liabilities while managing contribution volatility, liquidity needs and governance constraints. Although both plan types are liability-driven in principle, their asset allocation frameworks often diverge.

Pension plans typically have larger pools of assets and more mature governance structures, while OPEB plans frequently contend with lower funded ratios, less certain cash flow patterns and health-care-related actuarial variability. Public pension plans have broadly diversified away from traditional stock and bond portfolios toward a wider mix of alternative investments and opportunistic fixed income, while higher interest rates are prompting renewed attention to fixed income.

The institutional objectives, constraints and evolving allocation practices of public pension and OPEB plans are central to achieving their long-term outcomes. As part of this process, we provide an overview of the steps we believe will support successful asset allocation, including integrating asset-liability analysis, funded status considerations and liquidity management into a coherent policy framework.

The Importance of Asset Allocation

Asset allocation is the most consequential long-term investment decision for public pension and OPEB trusts. It shapes expected return, funded status volatility, contribution requirements and the ability of governmental entities to meet benefit obligations over time. For public plans, asset allocation cannot be evaluated in isolation from actuarial assumptions, contribution policy, plan maturity, liquidity demands and sponsor risk tolerance. Unlike other investment pools, public pension and OPEB fiduciaries must align investment strategy with liabilities that extend across decades.

Public pension plans have shifted over time from portfolios concentrated in public equities and core fixed income toward more diversified allocations that include private markets and other alternatives. Broader institutional studies similarly show that public investors increased alternatives exposure over the last five years, while recent trends suggest the higher interest rate environment has renewed interest in fixed income and reduced the pressure to reach for return through illiquid assets1. At the same time, actuarial and plan governance emphasizes that investment policy should remain tied to liability characteristics and funding discipline rather than simply following investment allocations of peers.

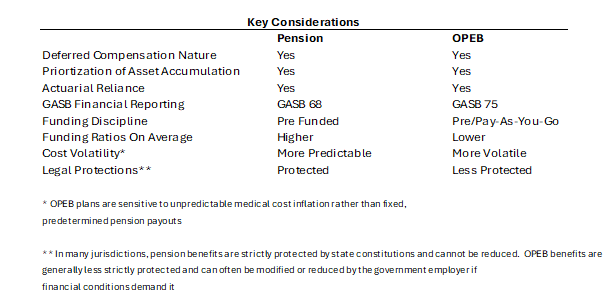

Core Structural Differences

Public pension plans and OPEB plans both sponsor specific post-employment benefits, yet their liabilities differ in important ways that influence asset allocation. Pension liabilities are generally linked to salary history, service, mortality and retirement timing. While these factors are complex, they are usually more stable and easier to model than retiree health-care costs. OPEB liabilities, by contrast, are affected by medical trend assumptions, plan design changes, utilization patterns and coverage elections, all of which introduce additional uncertainty. As a result, OPEB plans often exhibit more assumption risk and more potential variation in projected benefit obligations.

Funding policies also differ. Many public pension systems operate with established contribution frameworks, dedicated assets and relatively mature governance processes. OPEB arrangements vary more widely; some are prefunded in trust, while others remain largely pay-as-you-go or only partially funded. This distinction matters because a less funded OPEB plan may have a shorter effective horizon, greater dependence on sponsor contributions and lower tolerance for illiquidity. In practice, this often leads OPEB fiduciaries to place more weight on liquidity, downside protection and flexibility in contribution planning.

These differences do not imply that OPEB portfolios should always be conservative or that pension portfolios should always be aggressive. Rather, they suggest that strategic allocation should reflect the specific plan’s funded status, benefit payment profile, sponsor capacity and governance ability. A well-funded, professionally governed OPEB trust may support meaningful growth exposure, while a mature pension plan with rising negative cash flow may need to moderate illiquidity and rebalance toward income-producing assets.

Core Asset Allocation Framework

Asset/Liability Awareness

An effective asset allocation framework for public pension and OPEB plans aligns liability needs with capital market expectations. Asset-liability studies remain the primary tool for evaluating how various portfolios affect funded status, contribution volatility and the probability of achieving long-term return assumptions.

Several factors are particularly important:

- Funded status. Better-funded plans can often afford to emphasize downside protection and contribution stability, whereas less funded plans may feel pressure to maintain higher return-seeking allocations.

- Plan maturity and cash flow. Plans with potential high benefit payments relative to assets must be more attentive to liquidity, rebalancing needs and the risk of forced sales during stressed markets.

- Governance capacity. Complex allocations to private markets or hedge funds, as an example, may improve diversification on paper, but only if it can be supported by a sound governance structure to oversee manager selection, pacing, valuation, benchmarking and operational risk.

- The relationship between the investment return assumption and the strategic portfolio. A plan should not simply assume a target return and then back into a risky portfolio without considering whether the associated volatility and illiquidity are acceptable.

From this perspective, strategic asset allocation is a balancing exercise among growth, liquidity and implementation practicality. Public equity remains an important source of long-run growth and liquidity. Fixed income supports cash flow, diversification and, in a higher-rate environment, more meaningful expected returns. Real assets can support diversification and inflation sensitivity while private equity and private credit, as an example, may enhance return potential but reduce transparency and liquidity. The appropriate mix depends less on fashion and more on how each asset class contributes to the plan’s total risk budget and liability objectives.

Ongoing Challenges

Issues Influencing Asset Allocation Decisions

Several recurring challenges may continue to influence asset allocation decisions for public pension and OPEB plans, including:

- Assumed returns may exceed what markets can realistically deliver. When actuarial assumptions remain high relative to available opportunities, sponsors may feel pressure to adopt riskier portfolios, which can increase funding volatility.

- Liquidity management becomes more challenging as plans mature. Systems with significant benefit payments need dependable liquidity for monthly distributions, capital calls and portfolio rebalancing, especially during periods of market stress.

- OPEB plans face added uncertainty on the liability side. Healthcare obligations are often more sensitive to assumption changes and plan design revisions than pension obligations, which can amplify funded status volatility.

- Peer comparisons can be informative, but they should not drive policy. An allocation is not appropriate simply because it is common; it must fit the plan’s own liabilities, contribution structure, funded status and governance capacity.

Asset allocation for public pension and OPEB plans is fundamentally a liability-aware governance decision. The central objective is not merely to maximize return, but to build a portfolio that can support potential benefit obligations, manage contribution risk, preserve liquidity and remain executable through changing market conditions. Public pension plans have generally responded to the last two decades by broadening diversification and increasing alternatives exposure, yet the current higher-rate environment is reopening the case for fixed income. Because OPEB plans have varied funding structures and less certain liabilities, their investment policies must be aligned carefully with both investment and broader financial objectives.

We believe the most effective allocation frameworks combine asset-liability awareness, realistic capital market assumptions, liquidity planning and governance structures that are equal to the complexity of the portfolio. For both pensions and OPEB, long-term success may depend on maintaining a disciplined connection between liabilities, funding policy and investable strategy.

For more information on how these considerations may apply to your plan, please contact the professionals at Fiducient Advisors to discuss your asset allocation strategy and long-term objectives.

1Boston College Center for Retirement Research (CRR)

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.