As cash balance plans continue their rapid expansion, particularly among professional services firms, closely held businesses and partnerships, defined benefit Plan Sponsors are increasingly focused on investment strategy as a core component of plan success. One topic drawing more attention is the use of multiple investment pools within a single ERISA cash balance plan. While this structure can offer appealing design flexibility, it also introduces administrative, fiduciary and cost considerations.

This article examines the key tradeoffs of offering multiple investment pools in an ERISA cash balance plan and provides Plan Sponsors with practical guidance on whether this structure aligns with their objectives.

Why Multiple Investment Pools Are Even On the Table

Traditionally, pooled ERISA cash balance plans have relied on a single investment strategy aligned with the plan’s interest crediting rate (ICR) design. For example, plans using a market-based ICR often invest plan assets in a conservative portfolio that balances the capital preservation provision with growing participant accounts (e.g., a 60/40 allocation, or diversified income and growth strategy).

However, as stakeholder groups within organizations grow more diverse (equity partners vs. income partners, founders nearing retirement vs. younger cohorts or professional service firms with multiple practice areas) there is a growing demand to address differing objectives, including:

- differentiated risk exposures

- tailored investment horizons

- individualized economics

- more flexibility with customized strategies

Multiple investment pools can help address these differences.

Benefits of Using Multiple Investment Pools Customization for Participant Cohorts

For Plan Sponsors, one of the most frequently cited differentiators of adopting multiple investment pools is the ability to tailor investment risk across distinct participant groups within the plan. For example:

- Senior partners nearing retirement may benefit from a more conservative pool designed to reduce volatility. Or, alternatively, if senior partners commonly take advantage of a plan’s early withdrawal provisions, it may be appropriate to exclude their risk/return preferences when considering overall investment allocation(s).

- Younger partners or newly admitted equity members may prefer a growth‑oriented pool that seeks higher long‑term returns to help fund up to the maximum limit.

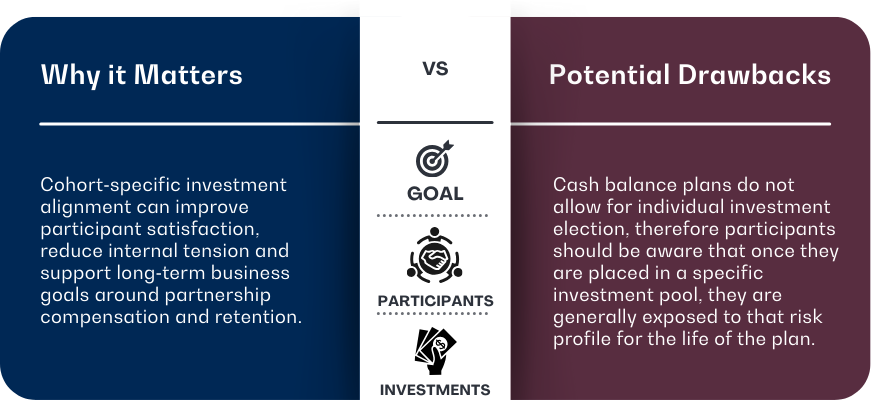

By aligning investment risk with demographic differences, Plan Sponsors may create a plan structure that feels more equitable and better aligned with participants’ individual financial situations and time horizons.

Improved Alignment with Market‑Based Interest Crediting Rates

With market-based cash balance plans, interest is typically credited to participants based on the actual investment returns from a single pool of plan assets. With risk-specific pools, each participant’s credited interest rate is determined by the performance of the particular pool they are invested in. This arrangement gives participants greater flexibility to customize their cash balance plan investments, allowing them to better match their individual financial goals and risk tolerance levels.

Maximizing tax deferrals and growing balances to the Section 415 maximum limit are the core goals of these plans; however, these objectives can often conflict. Tailored solutions better allow participants at different stages to potentially determine the appropriate levels of risk and return necessary to effectively maximize the tax deferred benefit and reach the maximum allowable balance.

Multiple investment pools help ensure that each participant group’s credited interest rate is supported by an investment strategy appropriate to that crediting method.

Enhanced Risk Management

Using multiple investment pools can create opportunities to manage risk more precisely:

- Plans with a wide range of ages, compensation levels or benefit formulas may face different economic sensitivities.

- Separate pools reduce the likelihood that one participant group’s investment performance disproportionately influences the economics of the entire plan.

- More tailored solutions allow participants to better manage their overall investment objectives including adjusting their 401(k) plan and other investments around their cash balance plan investment strategy to achieve their desired outcomes.

Additionally, at the total plan level, if younger participants allocate to a higher‑risk pool that underperforms, the Plan Sponsor can limit the impact of those losses to that group rather than exposing the entire participant population, particularly older participants at or near distribution.

Improved Transparency and Participant Autonomy

Multiple investment pools, particularly when paired with daily participant‑directed interest crediting, can create a more transparent and understandable economic relationship between asset performance, benefit growth and long-term retirement outcomes.

This is especially valuable for partnership‑based businesses where compensation, capital accounts and retirement benefits can be interconnected.

Drawbacks and Challenges of Multiple Investment Pools

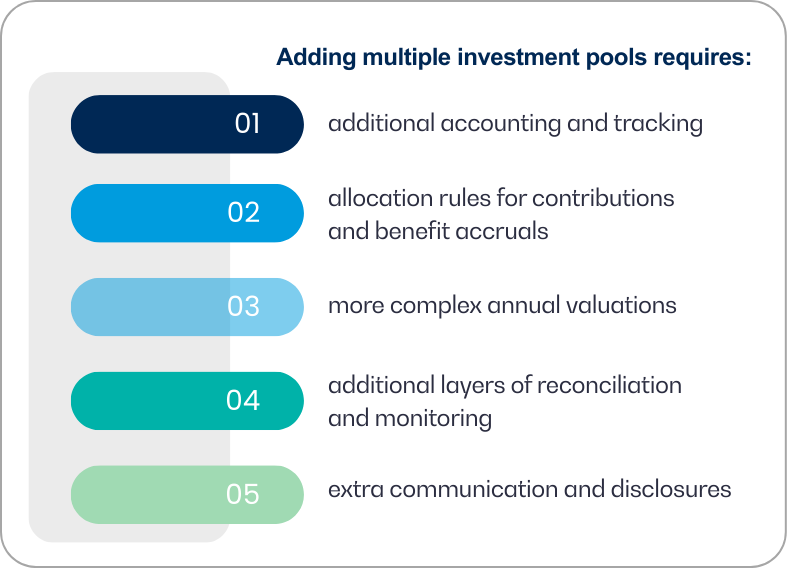

While the appeal of customization is strong, Plan Sponsors must carefully evaluate downside risks. Multiple investment pools introduce complexity both operationally and from a fiduciary standpoint.

Greater Administrative Complexity

Most traditional defined benefit plan recordkeepers and actuaries are not optimized to support multi-pool environments. Engaging a fiduciary advisory firm with expertise in professional service cash balance plan design can help Plan Sponsors manage these complexities, though often with additional cost or administrative requirements.

ERISA fiduciaries must assess whether the additional expenses are reasonable relative to the benefits provided. For smaller or mid‑sized cash balance plans, the financial impact may be material. Plan sponsors should carefully evaluate which expenses will be borne by the cash balance plan and which will be covered by the sponsoring entity.

Result: Administrative and actuarial complexity is one of the biggest friction points and often the deciding factor for Plan Sponsors.

Heightened Fiduciary Responsibility

Offering multiple investment pools inherently increases fiduciary burden:

- Each pool must be prudently selected and monitored

- Performance, fees, benchmarks, risk metrics and lineup suitability must all be evaluated separately

- Policies governing participant eligibility, election timing and re‑allocation rules must be clearly defined and consistently applied

Policies governing participant eligibility, election timing and re‑allocation rules must be clearly defined and consistently applied

If cash balance plan participants are allowed to select among investment pools with materially different risk levels, Plan Sponsors must ensure that disclosures and participant education are sufficiently robust to meet ERISA fiduciary standards for informed decision‑making.

Each pool must be prudently selected and monitored

Performance, fees, benchmarks, risk metrics and lineup suitability must all be evaluated separately

In short: While additional investment pools increase fiduciary oversight requirements, engaging in the right vendors can help to materially defray these risks.

Potential for Inequitable Outcomes or Participant Confusion

Introducing choice into a cash balance plan can create confusion among plan participants accustomed to defined benefit plan‑style simplicity.

Risks include:

- Misunderstanding how investment performance affects hypothetical cash balance accounts.

- Misalignment between selected risk level and participants’ long‑term goals.

- Dissatisfaction if one investment pool materially underperforms or outperforms another.

Even among sophisticated partners in law, medical, consulting and other professional service firms, investment choice within a defined benefit cash balance plan is not always intuitive and may require ongoing education to avoid poor outcomes. Transparent, upfront communication can be the difference between a successful plan design and one that creates confusion.

When Multiple Investment Pools Make Sense

Multiple investment pools can be a strong fit for:

- Large professional service firms with diverse equity partner demographics.

- Plans using market‑based ICRs that want to “match” investment pools to interest crediting options.

- Highly capital‑efficient partnership structures where retirement benefits are a core part of

total compensation. - Plan Sponsors committed to ongoing fiduciary oversight and willing to take on added administration.

In contrast, single‑pool structures generally remain more appropriate for:

- smaller plans

- firms with homogeneous participant demographics

- Sponsors seeking simplicity and cost efficiency

- plans approaching termination or de‑risking

In Closing

Multiple investment pools within ERISA cash balance plans can offer meaningful flexibility and more closely align investment strategy with participant demographics and interest crediting structures. However, this customization also introduces administrative, fiduciary and cost complexities. Plan Sponsors should evaluate not only the potential benefits, but also the long‑term governance needs and operational demands.

As cash balance plans continue to evolve, the decision to implement multiple investment pools should be guided by a clear strategic rationale, disciplined fiduciary processes and a thorough understanding of plan demographics and objectives.

Considering multiple investment pools in your cash balance plan? Understanding the fiduciary, administrative and operational implications is critical. Dive deeper into why the right investment partner can make all the difference and connect with Fiducient Advisors to discuss how a tailored investment strategy can support your plan’s objectives.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.