Over the years, my colleagues and I have had the privilege of working alongside hundreds of nonprofit investment committees across the country. These committees are often composed of thoughtful, accomplished individuals who care deeply about the organizations they support. And yet, even among the most capable groups, a potentially costly challenge can emerge.

It is not a lack of intelligence or commitment. It is a matter of focus.

Investment committees that lack intention and purpose may become hyper-focused on a benchmark, outperforming a peer institution or short-term relative results. While these comparisons may be useful reference points, they can quietly become the objective… and pull attention away from what truly matters.

These pools of capital were not created to optimize quarterly outcomes or validate decision makers. They exist to provide continuity and resilience, enabling organizations to pursue their mission through market cycles, leadership changes and moments of uncertainty.

When Expertise Becomes a Distraction

It is important for even the most capable investment committee members to guard against a natural tendency to default to the frameworks they know best. This tendency is especially understandable when committees include investment professionals. These individuals often bring valuable experience, strong instincts and a deep understanding of markets. But the scorecards that work well in traditional investment environments don’t always translate cleanly to nonprofit organizations designed to exist in perpetuity.

An individual overseeing an endowment portfolio is not managing capital for a career cycle, a compensation structure or a client who can change course at will. They are stewarding resources intended to support a mission across decades, often well beyond the tenure of any current committee member.

The risk is not poor intent or lack of sophistication it is that portfolios can gradually become optimized to solve the wrong problem.

The In Perpetuity Horizon Changes the Conversation

An in perpetuity, or simply very long term, time horizon should serve as a backdrop for every major investment decision. It influences how risk is defined, how liquidity is managed and how success is ultimately measured.

For nonprofits, risk is not simply underperforming a benchmark in a given year. The more meaningful risk is when it impairs the organization’s ability to deliver on its mission, especially during market stress, leadership transitions or unexpected challenges.

I strongly believe that investing is simple, but not easy. The foundational principles – diversification, rebalancing, discipline and cost vigilance – are well understood. The difficulty lies in applying demonstrated principles consistently when emotions, comparisons and recent performance threaten to cloud judgment.

Committees that anchor themselves in the organization’s time horizon tend to ask better questions:

• What rate of return should we target to advance our organization level goals (e.g., a new hospital wing, more scholarships, etc.)?

• How much volatility can we tolerate without disrupting spending?

• How liquid does the portfolio need to be in difficult markets?

• What tradeoffs are we willing to make between short term results and long-term sustainability?

These are not benchmark questions. They are mission questions.

Mission First, Portfolio Second

The most effective nonprofit investment committees reverse the traditional investment process.

Rather than starting with an index or peer group and asking how to outperform it, they begin with the mission. They clarify how the endowment or foundation is meant to support that mission, both today and far into the future. They define risk in those terms. Only then do they work backward to portfolio construction. This sequencing matters.

When mission comes first, the portfolio becomes a tool rather than a trophy. Asset allocation decisions feel different. Liquidity takes on greater importance. Even quarterly performance reviews become more productive, because the central question shifts from “Did we beat peers?” to “Is the portfolio tracking to what the organization needs it to do?”

Performance matters, but so do asset allocation, investment policy review, liquidity, cost analysis and more.

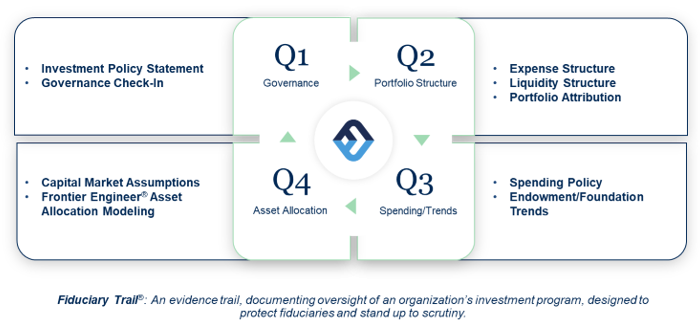

Utilizing a discipline such as Fiducient Advisors’ Governance Calendar helps committees systematically address these critical items over the course of the year. It also reduces the risk of becoming overly focused on short‑term results or reacting to the crisis of the day. By creating a structured cadence for governance discussions, committees are better positioned to remain disciplined, forward‑looking and aligned with the organization’s long‑term mission.

Below is an example of how our Governance Calendar can help structure an investment committee’s work across the year; ensuring that performance, policy, risk and stewardship responsibilities all receive appropriate and timely attention.

Guarding Against Our Most Human Instincts

It is easy, especially when a nonprofit’s mission tugs at your heart, to let human emotion creep into investment decisions. Committee members are volunteers, donors and advocates. Without realizing it, we can begin to view decisions affecting the endowment or foundation through a personal lens rather than that of the institution.

One of the most common expressions of this is the urge to time the market. Whether it is leaning in on risk in a strong market like we are experiencing today or pulling back risk after a downturn, market timing may feel prudent in the moment. In reality, it is one of the most emotionally driven, and consistently destructive, investment behaviors.

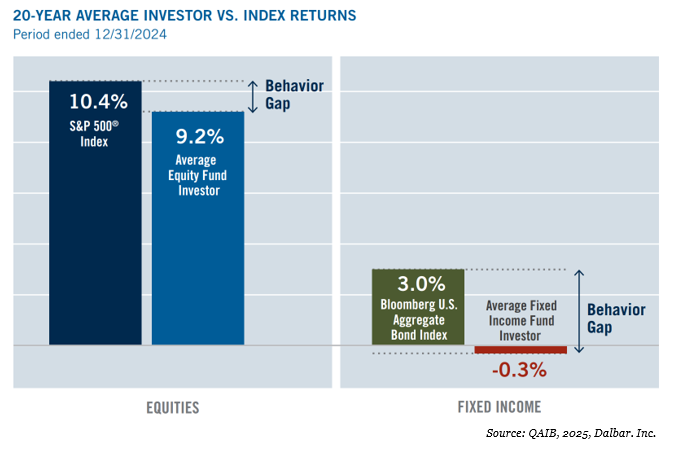

DALBAR’s long-running study estimates actual returns earned by the average fund investor. It finds investor-experienced returns often lag market benchmarks, reflecting the impact of behavior and costs, particularly the tendency to buy or sell at inopportune times.

The Cost of Market Timing

For nonprofit investment committees, the lesson is especially important. Endowments and foundations exist precisely because they are designed to rise above those impulses; maintaining discipline through full market cycles in service of a mission that outlasts any single moment.

Guarding against these instincts doesn’t require predicting markets. It requires a strong plan, governance, clarity and humility, along with a commitment to act through the lens of the institution, not the individual.

The Steward’s Role Is Not to Be Clever

The nonprofits I’ve worked with that experience the most investment success tend to share a common practice: Their investment committee members choose stewardship over their own investment acumen.

Good stewards understand that some of the most challenging moments come after periods of strong performance. Rising markets can inflate confidence, mask risk and subtly encourage portfolios to drift toward complexity or overreach.

That responsibility includes having the discipline to push back when discussions become overly competitive or ego driven, and to recenter the conversation on mission and longevity.

A Final Thought

Nonprofit investment committees shoulder extraordinary responsibility. They are entrusted with honoring past generosity while enabling future impact; and with conditions that today are as uncertain as ever. Good committee members don’t need to be heroic; they need to be purposeful.

By starting with the mission, respecting the organization’s long-term horizon, and working backward to portfolio construction, committees can harness their expertise without it becoming a distraction. They can embrace the truth that nonprofit portfolios exist for two reasons and two reasons only: to sustain and advance the organization’s mission. Success is not measured by outsmarting a benchmark or outperforming a peer. It is measured by an organization’s ability to continue its work, faithfully and sustainably, for generations to come. To learn more about optimizing your committee’s effectiveness, feel free to contact me or any of the professionals at Fiducient Advisors.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.