Kevin Warsh assumes the role of Fed Chair with growth and inflation trending in opposite directions

Key Observations

• Global equities continued to push higher in May, bolstered by strong Q1 corporate earnings and an acceleration in enthusiasm surrounding AI. Emerging markets led the way, on the back of strong gains in Korea and Taiwan.

• Equity markets appear increasingly narrative-driven, which poses unique risks that are offset by an incredibly strong fundamental backdrop.

• Kevin Warsh assumed his role as Fed Chair in May. He steps into the role at a very difficult time for monetary policy. Going forward, the Fed will need to contend with a softening labor market and a concerning resurgence of inflation that is further complicated by ongoing geopolitical risks.

Market Recap

May extended the global equity rally as markets grew increasingly optimistic about a potential diplomatic breakthrough between the U.S. and Iran, and blockbuster technology earnings pushed major indices to fresh all-time highs. Although inflation data reminded investors that price pressures remain stubbornly persistent, risk appetite held firm as markets looked past near-term headwinds and focused on strong corporate fundamentals and the prospect of easing geopolitical risk.

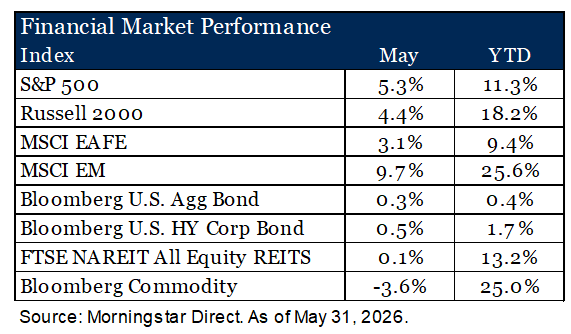

Large cap U.S. equities continued their advance. The S&P 500 Index returned 5.3% for the month, closing at a new record above 7,500, with the Nasdaq gaining more than 8%. Technology stocks were the dominant force as enthusiasm around the AI trade accelerated. Nvidia reported 85% year-over-year revenue growth, and shares of Dell surged over 30% on a strong earnings beat, reinforcing the broadening of the AI infrastructure narrative beyond chipmakers and into the full technology stack. Smaller companies also participated, though at a more measured pace. The Russell 2000 Index gained 4.4% and achieved a new all-time high, supported by a decline in Treasury yields and continued broadening of earnings growth into cyclical sectors like industrials and materials.

International equities also posted solid gains but trailed their U.S. counterparts. The MSCI EAFE Index returned 3.1%, with broad participation across both Europe and Japan. Emerging markets continued to stand out. The MSCI EM Index surged 9.7%, driven by continued strength in semiconductors and AI-related names across Taiwan and South Korea. EM equities are now up more than 25% year to date and more than 50% over the past year.

Fixed income returns were more muted, with the Bloomberg U.S. Aggregate Bond Index posting a 0.3% gain. Bond yields initially edged lower as geopolitical uncertainty weighed on growth expectations, but reversed course later in the month due to hotter-than-expected inflation data. Kevin Warsh officially assumed the role of Fed Chair in May, marking a leadership transition that markets will closely monitor. Warsh was sworn in at a difficult time for the Fed. April’s PCE reading (the Fed’s preferred measure of inflation) came in at 3.8% year-over-year, its highest level since mid-2023, and Q1 GDP growth was revised down to 1.6% from the initial 2.0% estimate. Against this backdrop, the April FOMC meeting minutes revealed the most internal dissent since 1992, with a majority of officials warning that rate hikes could become necessary if inflation continues to run above the 2% target. Credit markets delivered a more muted month relative to April’s rally. The Bloomberg U.S. Corporate High Yield Index returned 0.5% as spreads held largely stable.

Returns across real assets were mixed. The FTSE NAREIT All Equity REITs Index finished essentially flat for the month. Modestly higher interest rates, renewed inflation concerns and the prospect of tighter monetary policy offset strong results in lodging/resorts, which benefited from falling oil prices (i.e., cheaper cost to travel). Commodities meanwhile pulled back sharply. The Bloomberg Commodity Index declined 3.6%, driven primarily by a steep drop in crude oil prices. Oil posted its largest monthly decline since April 2025, falling nearly 17%, after the U.S. and Iran agreed to a 60-day memorandum of understanding that included plans to reopen the Strait of Hormuz and ease sanctions on Iranian oil exports. While diplomatic progress remains incredibly fragile, markets moved swiftly to reprice the geopolitical risk premium that had been embedded in energy prices since the start of the conflict.

Fed Facing Difficult Policy Path as Kevin Warsh Takes Over

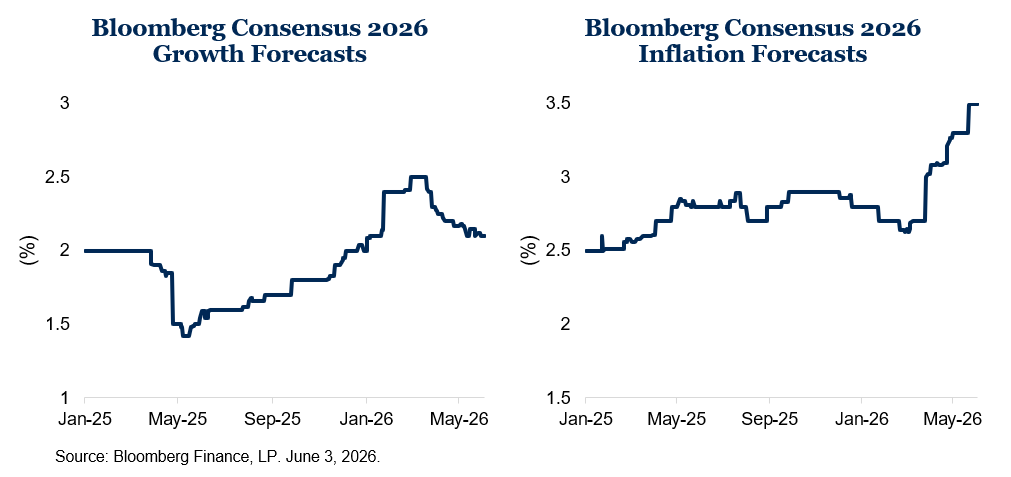

Kevin Warsh assumes the role of Fed chair at a difficult time for monetary policy. Warsh was widely expected to be more closely aligned with President Trump’s desire to bring interest rates lower, but the uncomfortable tension between rising inflation pressures and signs of softness in the labor market make a dovish pivot increasingly unlikely. Growth expectations have softened in recent months while inflation expectations moved higher, a combination that leaves the Fed with less flexibility and a narrower margin for error.

The divergent trajectories of growth and inflation complicate the Fed’s decision making. In a typical slowdown, weaker growth and a cooling labor market would give the Fed room to consider easing policy. Today, however, inflation is proving more persistent than many anticipated, and recent geopolitical developments have only added to that uncertainty. The result is a much more difficult environment for an incoming Fed chair, one in which the central bank remains focused on preserving its credibility in the fight against inflation and easing concerns about an encroachment upon its independence.

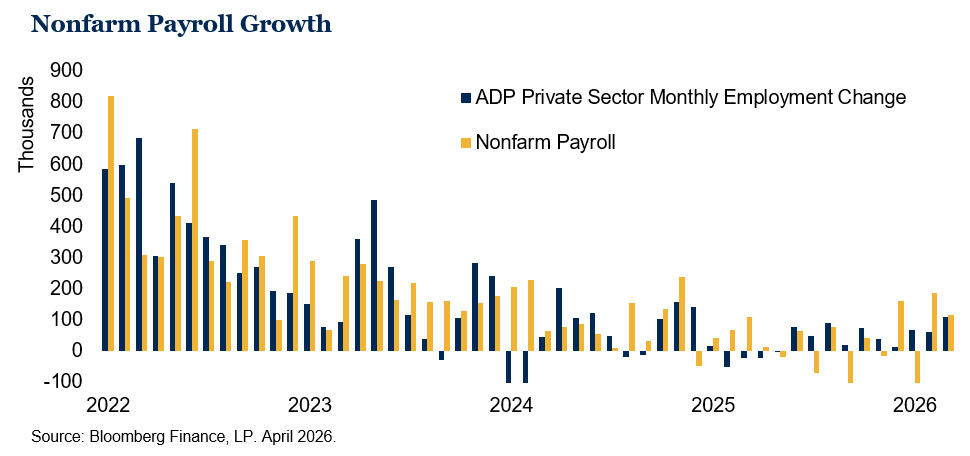

To further complicate matters, the labor market is also sending a mixed message. Hiring has shown signs of improvement, with relatively solid payroll growth in three of the last four months, but that rebound comes after a period of uneven and at times disappointing labor data. While the labor market has not broken down, it has shown enough softness to suggest that it needs to be handled with care. Recent improvements in jobless claims are encouraging and suggest some stabilization, but not necessarily a return to unambiguous strength.

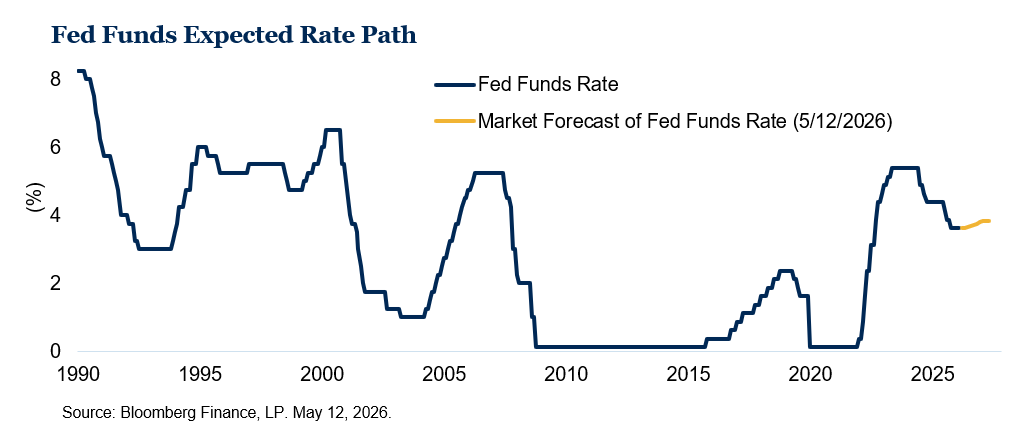

This combination of sticky inflation and a labor market that is holding up but not especially robust helps explain why the conversation around rate cuts has shifted so meaningfully. Earlier in the year, investors could reasonably argue that slowing growth might give the Fed room to move toward easier policy. That case has become much harder to make, and market expectations now reflect a much more restrained path for policy.

That is the situation Warsh is inheriting. He will be stepping into a role that demands a careful balance between competing risks. Move too quickly toward monetary easing, and inflation could become even more entrenched.

Stay restrictive for too long, and weakness in growth or employment could deepen. The external perception that the Fed’s independence may be compromised adds an additional layer of complexity to the beginning of his tenure.

Outlook

Equity performance in May was buoyed by accelerating enthusiasm for all things “Artificial Intelligence”, and the much-anticipated IPOs of companies like SpaceX, Anthropic and OpenAI will only serve to fan the flames. The recent rally in equity markets is supported by notably strong earnings growth, but longer-term stability will be dependent upon how effectively companies can translate AI investment into tangible improvements in earnings and profitability.

The fervor with which equity markets continue to push forward runs counter to some of the uncertainties emerging within the bond market, where a combination of stubborn inflation and persistently elevated budget deficits have put upward pressure on bond yields. Markets will be heavily focused on how the Fed responds to the increasingly complicated macro backdrop, while the approach of the mid-term elections could add another layer of uncertainty. Even so, we would be cautious about allowing political noise to overshadow the broader fundamental picture. With bond yields well above 4% in the U.S., the higher cushion from coupons is favorable and helps insulate portfolios against modest increases in interest rates.

We remain convicted that a balanced approach is crucial in the current environment. The excitement surrounding AI has fostered an element of short-termism and led to a market that is easily influenced by rapidly evolving narratives, which increases the risk of behavioral mistakes. We continue to favor an approach that is driven by the long-term fundamental drivers of return while remaining cognizant of evolving near-term risks.

Disclosures & Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses. Market returns shown in text are as of the publish date and source from Morningstar or FactSet unless otherwise listed.

- The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

- MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

- MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country.

- Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

- Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

- FTSE NAREIT Equity REITs Index contains all Equity REITs not designed as Timber REITs or Infrastructure REITs.

- Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification.

Material Risks

- Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and over longer periods of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

- International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country specific risks which may result in lower liquidity in some markets.

- Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

- Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class like leverage and/or industry, sector or geographical concentration. Declines in real estate value may take place for a number of reasons including, but are not limited to economic conditions, change in condition of the underlying property or defaults by the borrower.

- All investing involves risk including the potential loss of principal. Market volatility may significantly impact the value of your investments. Recent tariff announcements may add to this volatility, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance. You should consider these factors when making investment decisions. We recommend consulting with a qualified financial adviser to understand how these risks may affect your portfolio and to develop a strategy that aligns with your financial goals and risk tolerance.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.