On January 20, 2020, the first case of COVID-19 was diagnosed in the United States. As the virus continued to spread, many states issued stay-at-home orders, employers instituted work-from-home policies and the decade-plus bull market quickly reversed course. This not only impacted personal savings but also $6.3 trillion in retirement plan assets1.

Impact on Aggregate Retirement Savings

The sharp pullback in equity markets that occurred throughout March caused a relatively steep reduction of 11.2 percent in median participant account balances2. Concurrently, participants with larger account balances experienced greater losses than those participants with smaller account balances as periodic employee and employer contributions had a smaller impact in offsetting the negative market returns for participants with larger account balances.

Prior to the pandemic, the Employee Benefit Research Institute (EBRI) estimated a $3.68 trillion shortfall in aggregate for retirement savings within all U.S. households. Under EBRI’s most pessimistic scenario, the shortfall in retirement savings only increased by $412.8 billion or 11.2 percent3 due to the market, participant and Plan Sponsor action stemming from the pandemic. An equity market pullback was by far the largest contributing factor to the increased shortfall. By contrast, Plan Sponsor actions to suspend the matching contributions or increase eligibility requirements and participant decisions to reduce contributions for a year or take a one-time withdrawal were much less impactful than initially believed.

Participant Activity

During the second quarter, financial markets and, subsequently, 401(k) plan assets recovered swiftly. The muted participant activity over the period of volatility is equally positive.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act provisions provided retirement plan participants the flexibility to take qualified distributions, delay loan repayments and borrow up to 100 percent of their vested account balance. However, despite these provisions, there were no significant outflows of assets from 401(k) plans. Approximately 3.6 percent4 and 4.5 percent5 of participants on Fidelity’s and Vanguard’s platform, respectively, took a CARES distribution. Additionally, less than one percent of participants requested a CARES loan5.

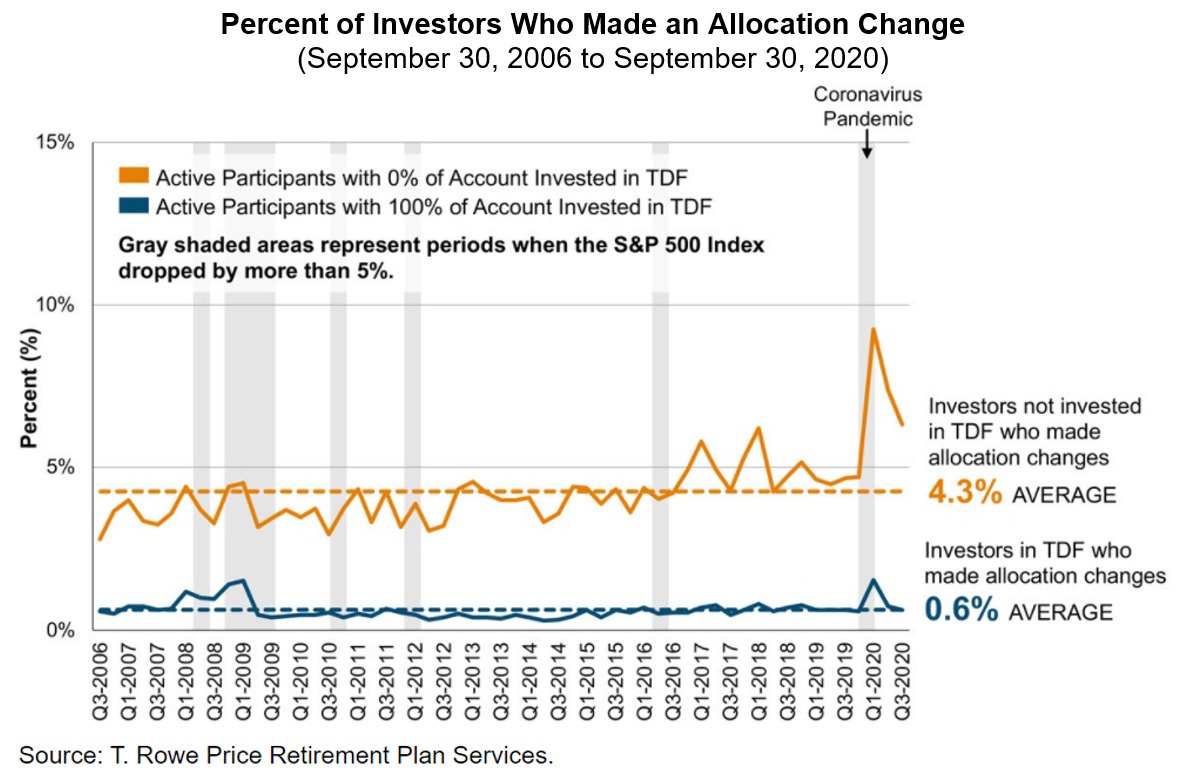

Another encouraging development was the low volume of investment-related activity. Only 8.1 percent of participants made any investment related changes so far this year compared to 5.3 percent last year. Over 97 percent of participants solely invested in target date funds stayed the course and did not make any changes to their investments, allowing them to fully participate in the subsequent market recovery.

What’s Next?

Unprecedented fiscal and monetary stimulus kickstarted the economic and financial market recovery. But this recovery is still fragile and uneven at best. With the number of positive cases on the rise, this pandemic is nowhere near the end.

At the same time, there is reason for optimism. If the high call volumes and number of account logins reported by recordkeepers serve as any evidence, many participants are engaged and plugged into their retirement savings. Plan Sponsors could use this unique opportunity to continue educating participants about the importance of retirement savings and prudent investment. This may also be an opportune moment to consider an advice or financial wellness offering to further help participants navigate these uncertain times.

For more information, please contact any of the professionals at Fiducient Advisors.

1 https://www.ici.org/policy/retirement/plan/401k/faqs_401k?con

2 Morningstar: Keep Your Distance 401(k) Participant Investment Behaviors (So Far) During the COVID-19 Crisis

3 EBRI: How the COVID-19 Pandemic Could Impact Retirement Income Adequacy for U.S. Workers

4 Fidelity: Leading through Uncertain Times, Volume 8, October 2020

5 Vanguard: COVID-19, the CARES Act, and plan participants’ response

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.