It’s no secret that COVID-19 altered the world as we know it, including the investment universe. In fact, over the last several months, the pandemic has shaped the way we work, the way we interact with each other, the way we spend money and the way we invest. With ESG (environmental, social, governance) investing already trending upward pre-pandemic, this public health crisis and its subsequent economic impact seems to have accelerated this development with no signs of slowing. U.S. sustainable funds garnered $7.3 billion in new assets in the first quarter of 2020, a quarterly record and more than half the amount of inflows during the entire 2019 calendar year.1

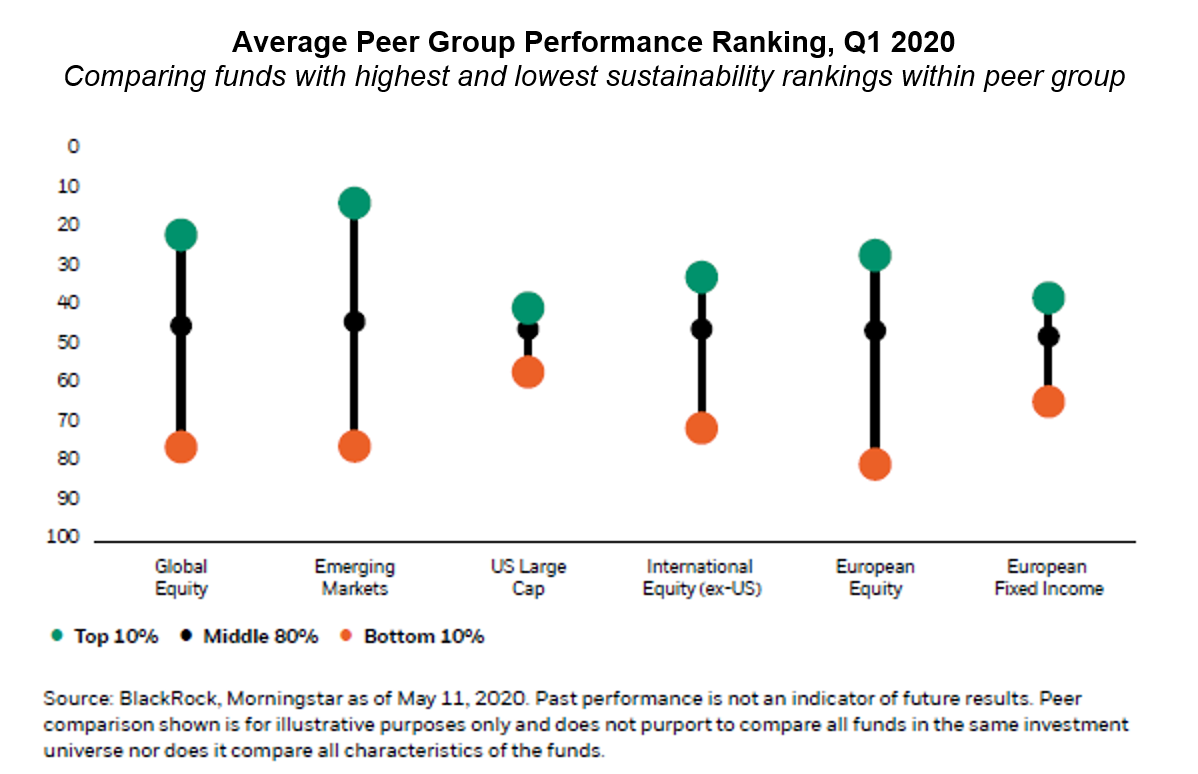

When we look back on the history of ESG investing, there was a long-held belief that investing in ESG strategies and strong performance were mutually exclusive – that in order to invest “responsibly,” investors had to sacrifice performance. As the landscape changes and data becomes more robust, that belief is increasingly being challenged. Convincing support of this is BlackRock’s assertion that during the severe market downturn in Q1 2020, 94 percent of “sustainable indices” outperformed their non-sustainable counterparts. These indices also exhibited outperformance during the previous market downturn in Q4 2018, with 75 percent of sustainable indices outperforming. As shown in the chart below, beyond sustainable indices, BlackRock’s findings indicate that funds scoring in the top 10 percent according to Morningstar’s sustainability ratings significantly outperformed funds ranking in the bottom 10 percent during the recent market pullback.

What Critics Say About ESG – And Why They Are Wrong

Oftentimes, critics of ESG and sustainable investing point to outperformance/underperformance as an “energy story,” stating that sustainable funds and indices outperform during periods when energy struggles, and vice-versa. BlackRock addressed this issue directly in their research, acknowledging that although a lower allocation to energy did contribute to relative results in Q1, a greater overall cause of relative outperformance was stock selection – higher exposure to more sustainable companies.

Other critics make a similar argument, asserting that, for the most part, technology exposure boosted recent ESG outperformance. However, Morningstar’s Jon Hale confirms that an overweight to the technology sector in itself did not provide much benefit to ESG funds; in actuality, it was exposure to specific stocks within the tech sector that scored well on ESG metrics, such as positive treatment of employees, that improved relative returns.2

Overall, across sectors, companies that exhibited more positive ESG characteristics fared better than their non-ESG counterparts during the Q1 market decline.

The Pandemic’s Effects on Consumer Habits

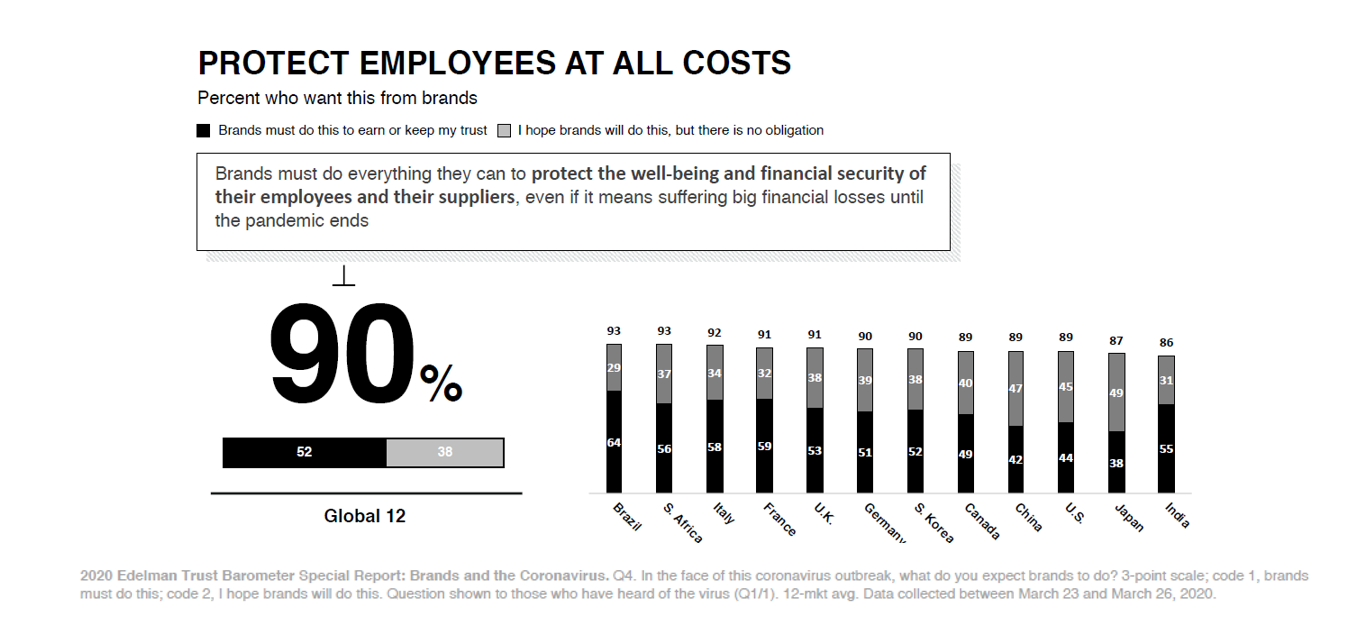

As a result of the COVID-19 pandemic and its unprecedented challenges in this modern age, ESG investors place even greater emphasis on the social and governance aspects of their ESG strategies. The Edelman Trust Barometer 2020 Special Report shows just how strongly consumers care about corporate responsibility in the current environment.

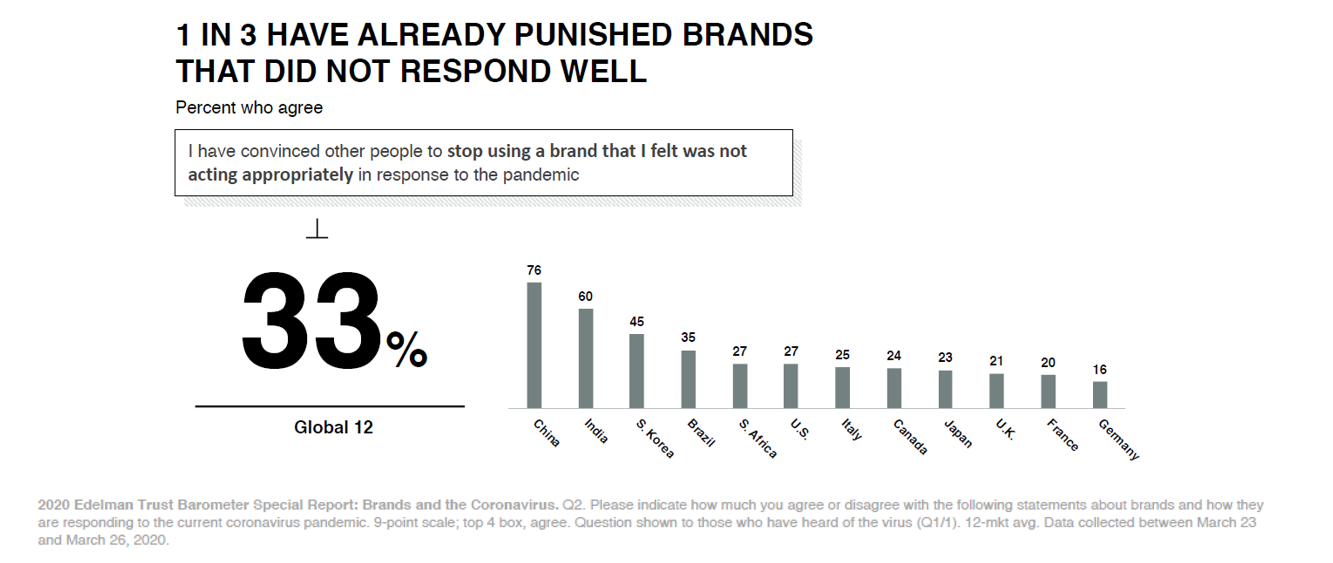

In that sense, each and every data point in the report points to the same conclusion: consumers expect the companies behind their favorite brands to be good corporate citizens, and even the most dedicated of customers will respond swiftly when that is not the case. Almost all survey respondents (90 percent) expect their brands to protect the well-being and financial security of their employees and suppliers during the pandemic even if it results in financial loss, and 33 percent of respondents have convinced other consumers to stop using a brand they felt was not responding appropriately to the pandemic.3

We, as investors, are well aware that consumer preferences will ultimately be reflected in stock prices, which suggests that companies exhibiting strong social and governance practices may ultimately be better positioned for success in the future.

COVID-19’s Effect on the Environment

While in the investment world, this pandemic seems to be having the most significant impact on the social and governance aspects of ESG investing, “shelter-in-place” and other similar “stay-at-home” orders imposed to limit the spread of COVID-19 have had a substantial impact on the environment as well. Carbon emissions have decreased dramatically, and the less frequently discussed nitrogen dioxide and particulate matter pollution levels have also decreased considerably.

The result? Significant improvement in air quality, so much so that in April, residents of northern India reported the Himalaya Mountains were visible from 125 miles away, which had not been the case for 30 years. Some animal life seems to be thriving in many parts of the world too, as leatherback sea turtles experience a revival in Florida and Thailand, goats “invade” a town in Wales and coyotes are on the prowl throughout the streets of San Francisco. Such developments might encourage the broader populace, including investors, to seek continued environmental recovery by supporting companies that advocate for, and even demonstrate, positive environmental practices moving forward.

Politics Surrounding ESG Strategies

Despite mounting evidence that both investors and consumers care about ESG factors, in June of this year, the U.S. Department of Labor issued a new proposal designed “to make clear that ERISA plan fiduciaries may not invest in ESG vehicles when they understand an underlying investment strategy of the vehicle is to subordinate return or increase risk for the purpose of non-financial objectives.”4 The general purpose of the proposed rule is to tighten the restrictions associated with utilizing ESG strategies in retirement plans. The proposal is subject to public comment and amendment, so it may not be passed as-is, or, it may not be passed at all.

Even though ESG investing seems politically charged and can be either supported or opposed by individual administrations, the long-term trend in the marketplace is toward sustainability. Investor flows into ESG strategies have increased year-over-year, regardless of which political party has occupied the White House or controlled Congress. Furthermore, performance metrics may suggest that incorporating ESG characteristics into one’s investment process is, in and of itself, evidence of fiduciary responsibility.

ESG Is Here to Stay

It is clear that the pandemic has dramatically altered the world in which we live, in nearly every possible way. The impressive economic and social effects resulting from COVID-19, from the original shelter-in-place measures to the ongoing social-distancing guidelines, will be felt for months and possibly years to come. This worldwide crisis is forcing people everywhere to evaluate interaction between citizens and corporations, determining the overall impact our actions have on the global community. In such an environment, ESG investing is likely to become even more important.

For more information, please contact any of the professionals at Fiducient Advisors.

Devon Francis is Partner and Senior Consultant of Fiduciary Investment Advisors, LLC which is a wholly owned subsidiary of Fiducient Advisors

1 BlackRock, “Sustainable investing: resilience amid uncertainty.” May 18, 2020

2 Caitlin McCabe – Wall Street Journal. “ESG Investing Shines in Market Turmoil, With Help From Big Tech.” May 12, 2020. https://www.wsj.com/articles/esg-investing-shines-in-market-turmoil-with-help-from-big-tech-11589275801

3 Edelman, “2020 Edelman Trust Barometer Special Report: Brands and the Coronavirus.” March 30, 2020. https://www.edelman.com/sites/g/files/aatuss191/files/2020-03/2020%20Edelman%20Trust%20Barometer%20Brands%20and%20the%20Coronavirus.pdf

4 Plan Adviser, “DOL Proposes Stricter Rules About ESG Investing in Retirement Plans.” June 24, 2020. https://www.planadviser.com/dol-proposes-stricter-rules-esg-investing-retirement-plans/

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.