With the increase in high deductible health insurance plans, Health Savings Accounts (HSA) have seen a significant jump in utilization. An HSA provides a unique combination of tax benefits, withdrawal options and investment opportunities that can make it a valuable retirement savings account. Despite the increased popularity of the HSA, few individuals understand how to maximize the value of these accounts, especially for retirement planning.

What is an HSA?

An HSA is a type of savings account allowing an individual to save and invest money with preferential tax treatment to pay for current and future medical expenses. Though you can use the funds in an HSA to pay for medical expenses at any time, you can only contribute to an HSA if you have a High Deductible Health Plan.

For calendar year 2020, individuals can contribute $3,550 and families can contribute $7,1001. Unlike Flexible Spending Accounts (FSA) there is no “use it or lose it” feature. A balance in an HSA can be carried forward year after year. This feature, combined with the ability to invest HSA assets, creates the potential to develop significant account balances over time.

Benefits from Investing

Though HSAs are savings accounts, the majority of HSA vendors allow for a portion of the account balance to be invested, and compounding returns can help accumulate high balances. Let’s look at a 25-year-old individual who is saving the maximum into their HSA each year. If this person took no withdrawals and let the money sit in cash assuming a zero percent return, by the time they reach retirement at age 65, their account would be worth $145,550. This example also assumes that contribution limits are never increased. If we look at the same individual with the same assumptions but allocate the account to an investment earning a rate of return 7 percent annually, the ending account balance would be $761,864. Understanding the benefits of investing, as well as the withdrawal strategies discussed below can really maximize the value of a Health Savings Account.

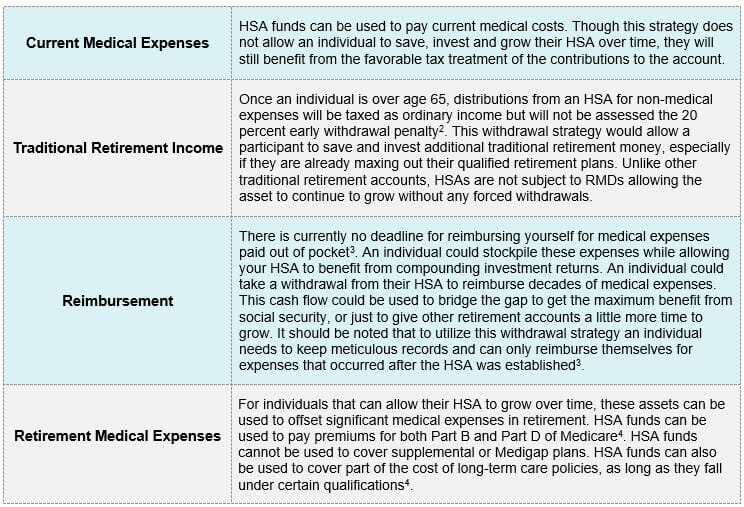

Withdrawal Strategies

Understanding the withdrawal strategies below can help individuals maximize the benefits of an HSA.

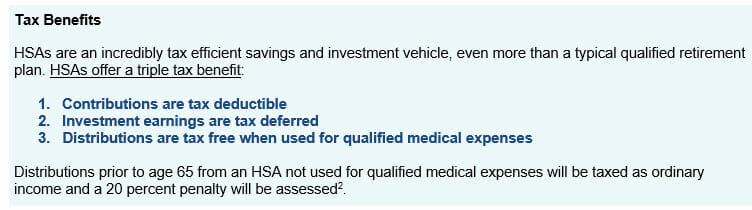

In summary, the triple tax benefits of an HSA create a tax efficient, flexible and dynamic account that can have a meaningful financial impact for people both in retirement and prior to retirement. Understanding the withdrawal strategies mentioned above and incorporating them into a full financial plan will help prepare savers for retirement.

For more information, please contact any of the professionals at Fiducient Advisors.

Gregory Adams is a Consultant of Fiduciary Investment Advisors, LLC which is a wholly owned subsidiary of Fiducient Advisors

1“Health Savings Account (HSA)” Healthcare.gov 2020

2Bobby Glotfelty “The Truth About HSAs and Retirement” Betterment.com January 27, 2020

3Kate Dore “Compound It! Being Smart with HSA Reimbursements” HSAstore.com 2017

4Fidelity Viewpoints “5 Ways HSAs can Fortify Your Retirement” Fidelity.com December 19,2019

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.