For individuals and families with significant wealth, medical expense planning is not just about covering costs. It’s about preserving capital, maintaining liquidity and ensuring healthcare needs are met without disrupting sophisticated investment strategies or generational wealth transfer plans.

Rising healthcare costs, increasingly complex insurance structures and the potential for unexpected medical events require a proactive and integrated financial approach. When addressed strategically, healthcare planning can be aligned with your broader wealth management objectives allowing you to protect your legacy while maximizing growth opportunities.

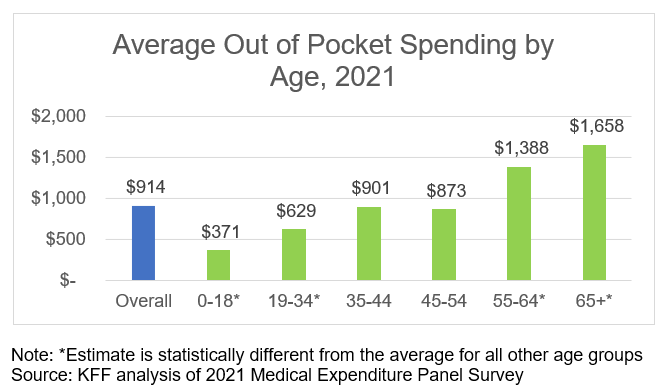

The Financial Impact of Medical Expenses

Healthcare costs can be one of the largest and most unpredictable expenses. Recent analyses estimate that Americans owe at least $220 billion in medical debt, with approximately 14 million people (6% of adults) owing over $1,000 and about 3 million people (1% of adults) owing more than $10,0001.

For high-net-worth households, the primary risk is not insolvency, but opportunity cost – being forced to liquidate investments at suboptimal times or reducing allocations to high-growth opportunities due to sudden cash flow demands. By building medical expense planning into your overall wealth strategy, you can preserve portfolio integrity while keeping liquidity available for strategic moves.

Strategies for Managing Healthcare Costs

1 – Understand and Optimize Insurance Coverage

A comprehensive understanding of your health insurance is the first step toward minimizing medical expenses. Review the specifics of your policy, including covered services, deductibles, co-payments and out-of-pocket maximums. Strategic adjustments, such as choosing a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA), can help you lower premiums while leveraging tax advantages. Supplemental insurance policies for dental, vision, or critical illness coverage can also fill gaps and reduce potential out-of-pocket costs2.

2 – Leverage Tax-Advantaged Accounts

HSAs and Flexible Spending Accounts (FSAs) are powerful tools for managing medical expenses while maximizing wealth. Contributions to HSAs are tax-deductible, and the funds grow tax-free, providing an opportunity to invest unused balances. Unlike FSAs, HSA funds roll over year to year, allowing long-term growth that aligns with your broader financial strategy. It can also be helpful to view your HSA account as an additional investment vehicle to supplement retirement planning3.

3 – Integrate Healthcare Costs into Financial Planning

For those focused on wealth maximization, planning for healthcare costs is non-negotiable. Allocate a specific portion of your monthly income for routine expenses like prescriptions, preventive care, and doctor visits. Additionally, maintain a well-funded emergency account earmarked for unexpected medical costs. This approach helps ensure that your long-term investments remain intact even during unforeseen financial strain4.

4 – Prioritize Preventative Care

Preventive care is one of the most cost-effective ways to manage healthcare expenses. Many insurance plans fully cover preventive services like annual check-ups, screenings and vaccinations. Staying proactive about health not only reduces future medical costs but also allows you remain in optimal condition to focus on wealth-building activities. From a financial perspective, investing in preventive care today minimizes expensive treatments in the future, preserving more capital for other investments.

5 – Explore Available Resources

If faced with substantial medical bills, explore all available resources. Healthcare providers often offer payment plans or discounts for upfront payments. Nonprofit organizations and government programs can provide additional assistance. Negotiating medical bills or working with financial advocates can also yield significant savings, ensuring that more of your resources remain dedicated to wealth generation5.

Aligning Medical Expenses with Investment Strategies

Medical expense planning should be integrated into your overall financial strategy. This involves assessing how healthcare costs impact liquidity needs, risk tolerance and long-term investment goals. For example, tax-advantaged accounts like HSAs can serve as both a safety net for healthcare costs and a component of your retirement portfolio.

For high-net-worth individuals, considering healthcare costs in estate planning is equally crucial. Establishing trusts or dedicating investment accounts to future medical expenses can provide additional financial security while permitting your overall wealth to continue to grow.

Securing Your Financial Future Through Proactive Planning

Healthcare costs are inevitable, but they do not need to derail your long-term objectives. By understanding your insurance coverage, leveraging tax-advantaged accounts, integrating healthcare into your financial plan, prioritizing prevention and optimizing available resources, you can protect your wealth and remain positioned for sustained growth.

Taking a proactive, integrated approach today can help ensure your financial health – and your legacy – are prepared for the unexpected.

For more information and financial planning advice, please contact any of the professionals at Fiducient Advisors and for further insights, please take a look at our 2025 Financial Planning Guide.

1The Burden of Medical Debt in the United States | KFF, February 12, 2024

2What is Supplemental Health Insurance? | Healthinsurance.org

3How to Plan for Rising Health Care Costs | Fidelity.com

4Report on the Economic Well-Being of U.S. Households in 2021 | Federalreserve.gov

5How to Negotiate Your Medical Bills | Time.com

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.