The importance and necessary steps to help ensure you are well positioned.

Importance of Life Insurance1

For high-net-worth individuals, having an effective life insurance plan is crucial not only for protecting your legacy but also for leveraging financial opportunities.

How High-Net-Worth Individuals Are Defined

The term “high-net-worth individual” (HNWI) typically refers to someone with at least $1 million in liquid assets, not counting their primary home. While this threshold can shift a bit depending on the financial institution or country, the focus is on assets that are readily accessible, like cash, investments or business interests.

Within the insurance landscape, being classified as a high-net-worth individual often has similar requirements, usually liquid assets north of that $1 million mark. However, HNWIs aren’t just identified by a number. Their compelling financial profiles often involve multiple investments, luxury properties, valuable collections or business interests that require specialized insurance solutions.

Insurers serving HNWIs frequently offer:

• Higher coverage limits

• Access to private client services

• Customized protection for fine art, jewelry, vintage cars or unique real estate

• Enhanced risk management strategies tailored to more complex lifestyles

Ultimately, both in general and for insurance purposes, the designation comes down to a combination of significant liquid wealth and a need for more personalized financial strategies. When most people think about risk management within their financial lives, they often think about diversification and allocation decisions. While those decisions are important, risk management does not stop with asset allocation, but more importantly leads us to critical insurance conversations and decisions. Life insurance can provide financial protection for loved ones and family. Appropriate life insurance planning can help achieve many common objectives from providing income replacement, meeting educational expenses, paying off debt or can assist with funeral and burial expenses. For others, it can also be a critical step to estate planning, providing liquidity to pay estate taxes or other expenses.

Beyond these personal benefits, life insurance plays a vital role for business owners as well. For those who own businesses, life insurance is not just about protecting family members, it’s a cornerstone of sound business continuity planning. It can help replace lost income, cover outstanding business debts, and ensure employees and partners are protected if an owner unexpectedly passes away. In businesses with multiple owners, life insurance can be structured into buy-sell agreements, giving surviving partners the ability to purchase the deceased’s share. This arrangement helps maintain business stability, prevents disruption and keeps control within the desired hands.

Whether your focus is on family, legacy or business, thoughtful life insurance planning can safeguard what matters most, both today and for generations to come. Additionally, it can provide you with peace of mind, knowing you have taken the necessary steps to protect your loved ones’ financial futures, even if you are no longer around to provide for them.

Role of Life Insurance in Business Succession Planning

For business owners, life insurance carries notable significance beyond personal financial protection. It often provides a critical foundation for business succession planning, helping ensure the enterprise you’ve built can continue to thrive, even in your absence. This type of coverage is typically used to create liquidity when it’s needed most, offering financial support to replace your lost income, pay off outstanding business loans or cover essential operating expenses.

In businesses with multiple owners, life insurance is frequently woven into buy-sell agreements. These arrangements enable surviving partners to purchase the deceased owner’s share seamlessly, which helps maintain the stability of the business and protects it from potential disruptions or intervention by external parties. By integrating life insurance into your succession planning, you help secure the ongoing success of your company, protect your employees’ livelihoods, and ensure your long-term vision is carried forward – no matter what unexpected events may arise.

When Should You Secure Life Insurance?

One of the most common questions from high-net-worth individuals is, “When is the right time to purchase life insurance?” While the short answer is that you can purchase coverage at any point, certain periods are especially well-suited to review your needs. Tax season, for example, is a natural opportunity; your financial information is organized, your investments are top-of-mind and you’re often having important discussions with your advisors. Using this momentum to assess your life insurance needs ensures your strategy remains aligned with your full financial picture, help maximizing protection for your family and legacy.

In general, the ideal time to secure life insurance is when you’re making major life or financial changes:

• Marriage or divorce

• Birth or adoption of a child

• Purchasing a new home

• Starting or expanding a business

• Significant investment changes or windfalls

• Estate planning updates

When these events occur, or even annually during tax season, it’s wise to revisit your coverage to make sure it fits your current and future needs.

By being proactive and aligning your insurance decisions with major financial milestones, or simply using the yearly rhythm of tax planning, you’re taking strategic steps to preserve your wealth, protect your family and reinforce your overall financial framework.

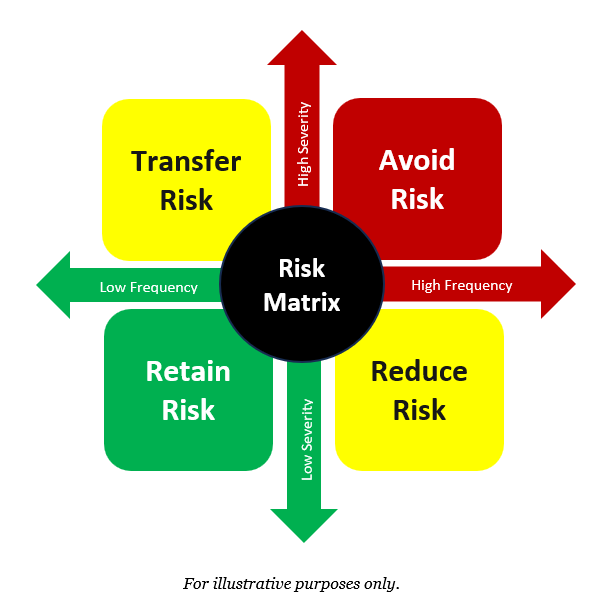

Review of the Risk Assessment Matrix

Life insurance falls in the ‘Transfer Risk’ portion of the matrix below, being in the Low Frequency & High Severity portion of the chart, with the primary objective being to protect your finances from significant risk exposure that could be detrimental to your family’s ability to survive financially upon your passing. Many typically handle this by transferring that risk to a third party, like an insurance company.

Essential Steps to Help Ensure your Life Insurance is Working to its Fullest Potential

1. Assess Your Coverage Needs

Your life insurance needs can be complex, especially when managing significant assets. Start by reviewing your current coverage to ensure it aligns with your financial goals and obligations. Typical coverage equates roughly to between 10 to 16 times your annual income. Consider additional factors such as:

- Debt Repayment: Confirm your policy covers outstanding debts, including mortgages and business loans.

- Estate Taxes: Evaluate whether your coverage can handle potential estate taxes to preserve your wealth for heirs.

- Income Replacement: Ensure adequate coverage to replace your income and maintain your family’s lifestyle.

Finding the right amount of coverage can seem overwhelming. Take time to consider your unique financial situation; think about not just your assets, but also your long-term obligations and any changes that might affect your family’s needs. A thoughtful assessment ensures your policy will be there to safeguard the lifestyle and legacy you’ve built.

2. Explore Different Policy Types

Not all life insurance policies are created equal. For high-net-worth individuals, exploring various types of policies can help maximize benefits:

- Term Life Insurance: Offers a death benefit for a specified term with no cash value accumulation. It is ideal for young families and adults who need insurance for a set number of years, in some instances mirroring the time until your expected retirement or final mortgage payments. Term life is also appreciated for its simplicity and affordability, making it a practical solution for those seeking to cover specific obligations, such as estate taxes or outstanding debts, within a predetermined period.

- Whole Life Insurance: Provides lifelong coverage with a cash value component that grows over time. It is more expensive but can be a good option if you want permanent insurance coverage and the opportunity to accumulate savings. The cash value portion acts as a tax-deferred savings vehicle, which can be an attractive option if you have already maximized contributions to other retirement accounts. Over time, you may borrow against or withdraw from the cash value to supplement retirement income or cover unforeseen expenses.

- Universal Life Insurance: Offers flexibility in premiums and death benefits, along with a cash value component. Unlike whole life, universal life policies allow you to adjust the amount and timing of your premium payments and modify your coverage as your financial needs change. This flexibility is valuable for high-net-worth individuals whose income or estate planning needs may fluctuate over time.

- Variable Life Insurance: Includes investment options within the policy, allowing for additional potential growth of the cash value. This structure lets you direct a portion of your premiums into a variety of investment vehicles, potentially increasing returns but also introducing more risk compared to other permanent life options.

Understanding the features of each policy type can help you choose the best fit for your financial strategy. By aligning your coverage with your broader wealth management goals and factoring in your unique circumstances, you can ensure your life insurance works harder for you and your loved ones. Take the opportunity to compare plan options from reputable providers, weigh the pros and cons of each, and consider how each policy type aligns with your goals – whether that’s maximizing growth, ensuring flexibility or providing for heirs. A comprehensive review today can help you confidently select coverage that fits your needs now and in the future.

3. Leveraging Life Insurance for Retirement Income

For individuals seeking creative ways to supplement retirement savings, a Life Insurance Retirement Plan (LIRP) may be a valuable addition to your financial toolbox. Unlike traditional retirement vehicles such as 401(k)s or IRAs, a LIRP utilizes a permanent life insurance policy (most commonly whole or universal life) to build up a cash value that grows tax-deferred over time.

Here’s how it works: As you pay premiums, a portion contributes to the policy’s cash value. Over the years, this cash value can accumulate, often at a steady rate, thanks to the policy’s underlying guarantees or market-linked performance (in the case of variable policies). The real advantage emerges in retirement, when you’re able to access these funds through policy loans or withdrawals, often on a tax-advantaged basis, to help bolster your income stream.

Some key benefits of incorporating a LIRP into your retirement planning include:

- Tax-Deferred Growth: Cash value growth inside the policy is not taxed as long as it remains within the policy.

- Tax-Advantaged Withdrawals: Funds accessed through loans may not incur income tax, provided the policy is properly structured and maintained.

- Estate Protection: The death benefit is usually passed on to beneficiaries income-tax free, helping secure your legacy and provide additional estate liquidity.

A LIRP may appeal to high-net-worth individuals who have already maxed out contributions to other retirement accounts and who appreciate both the protection and flexibility that life insurance can offer. As with any financial strategy, it’s wise to consult with your advisor to ensure this approach aligns with your broader retirement and wealth transfer goals.

3. Consider Riders2

Add-ons or riders can help enhance your policy. Common riders include:

- Accelerated Death Benefit: Allows you to access some of your death benefit if you are diagnosed with a terminal illness.

- Term Rider: Added to a whole life insurance policy to increase the death benefit for a certain amount of time (akin to additional Term Insurance).

- Guaranteed Insurability Rider: In some circumstances with Term Insurance, you will need to prove insurability to renew your policy after the term limit has ended. Some people want the assurance that they will automatically be insurable down the road, even if you develop a health condition since retaining the original policy.

- Waiver of Premium: Waives premiums if you become disabled and can’t work.

- Child Term Rider: Provides coverage for your children.

4. Help Optimize Your Policy for Tax Efficiency

Life insurance can help offer significant tax advantages, but proper planning is essential. For high-net-worth individuals seeking smart ways to preserve and grow wealth into retirement, life insurance can serve as a powerful tax planning tool. Certain permanent life insurance policies, including whole life, universal life and variable life, offer features that go beyond protection, with benefits designed to help boost your retirement strategy and optimize tax outcomes. Consider the following:

- Tax-Deferred Growth: Guarantee your policy’s cash value grows tax-deferred, enhancing its long-term value. The cash value component within permanent policies accumulates on a tax-deferred basis. This means your policy’s growth isn’t reduced each year by taxes, allowing you to potentially build a larger nest egg over time – much like the advantages seen in accounts such as IRAs or 401(k)s.

- Tax-Free Access: Many policies allow you to take loans against your accumulated cash value without being taxed as income, provided the policy remains in force. This can provide supplemental income in retirement, all while avoiding penalties and mandatory withdrawals associated with other qualified retirement accounts.

- Tax-Free Death Benefit: Confirm that the death benefit will be received tax-free by your beneficiaries. The death benefit typically passes to your beneficiaries income-tax-free under current IRS rules, making it a strategic tool to efficiently transfer wealth, especially when compared with some retirement accounts that may be subject to both income and estate taxes.

- Trust & Estate Planning: Explore placing your policy in an irrevocable life insurance trust (ILIT) to remove it from your estate, potentially reducing estate taxes. Particularly for those with large estates, combining life insurance with trusts (like an ILIT) can help remove the policy from your taxable estate, further reducing potential estate tax liability for heirs. With an ILIT, the trust (not you) owns the policy, which generally excludes the death benefit from your taxable estate. This can be especially helpful for individuals with larger estates who are concerned about estate tax liability. An ILIT also lets you specify exactly how and when the death benefit will be distributed to your beneficiaries, providing added control and protection. Keep in mind that once established, the terms of an ILIT cannot be changed, so careful planning is essential. This strategy can offer both valuable tax advantages and peace of mind that your wishes will be carried out as intended.

These advantages make life insurance an appealing complement for wealthy individuals looking to help minimize taxes both during retirement and in the transfer of assets to beneficiaries. Strategic layering of policies and regular policy reviews with your advisor help ensure your coverage continues to align with your evolving financial needs and long-term legacy goals.

Leverage Life Insurance for Philanthropy

For many with significant wealth, life insurance becomes more than just a tool to protect loved ones; it’s also a powerful way to give back and shape a legacy. There are several strategic ways high-net-worth individuals can harness life insurance for charitable giving:

- Naming a Charity as Beneficiary: One straightforward method is to designate your favorite nonprofit or foundation as a beneficiary of your policy. This allows you to provide a meaningful, often substantial donation to a cause close to your heart -without reducing the inheritance left to your family.

- Gift Policy Ownership: You may choose to transfer ownership of a policy to a qualified charitable organization like the American Red Cross or Habitat for Humanity. This often results in an immediate income tax deduction and, in some cases, ongoing deductions for future premium payments.

- Utilizing Trusts for Philanthropic Impact: Some opt to set up a charitable remainder trust (CRT) in tandem with life insurance. With this structure, you can support your philanthropic ambitions, reduce estate taxes and even provide income for yourself or loved ones during your lifetime.

- Tax-Efficient Legacy: Since life insurance death benefits are typically paid out tax-free, the full value of your intended gift goes directly to the organization, help maximizing your impact and simplifying the transfer.

If you’re passionate about philanthropy, weaving charitable giving into your life insurance strategy not only supports lasting change but can also create meaningful tax advantages for your estate and heirs.

5. Review Beneficiary Designations

Beneficiary designations play a crucial role in how your life insurance proceeds are distributed. Regularly review and update your beneficiaries to help ensure your policy aligns with your current wishes and estate plan. Consider naming primary and contingent beneficiaries to provide clarity and prevent potential disputes.

6. Conduct Regular Policy Reviews

Life circumstances and financial goals can change, making it essential to periodically review your life insurance policy. Schedule annual reviews with your financial advisor to:

- Update Coverage: Adjust coverage amounts as needed based on changes in your financial situation or family needs.

- Evaluate Performance: Assess the performance of any cash value components or investment options.

- Confirm Beneficiary Information: Make certain that beneficiary designations remain current.

In Closing

Effective life insurance planning is a cornerstone of a comprehensive wealth management strategy. While we do not sell insurance, we are happy to walk through this critical life insurance review with you and pragmatically review this process step-by-step to ensure you have a well thought out plan in place!

If you have questions or need assistance with a life insurance review, we’re here to help. Please contact a Fiducient Advisors’ team member to schedule a consultation and help optimize your life insurance strategy for your unique needs.

1Life insurance for high net worth applicants – Bankrate March 18, 2024

2What Are Life Insurance Riders? | 8 Common Types of Riders (insuranceblogbychris.com)

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.