Enduring wisdom on how to approach bear markets

There is nothing enjoyable about market corrections and/or recessions. They create fear, anxiety and uncertainty, potentially requiring a change in plans – like reduced spending in retirement or an unanticipated job search. Perspective can go a long way to successfully navigating these periods, uncomfortable and difficult as they may be. Outlined below is some enduring wisdom we can share having invested through bear markets and as students of history.

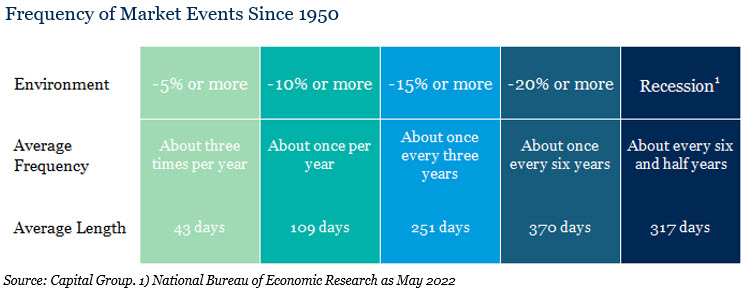

1 ) Corrections, bear markets and recessions are normal things

Volatility is an unfortunate but necessary evil in markets. Opportunity and volatility are irrevocably linked because without volatility, there would be no opportunity in investing. A similar comment can be made regarding recessions. They can both help reset expectations that become unreasonable at times and remove highly speculative (and often unproductive) activities that do not contribute to growing the economy. Reminding ourselves that these periods are normal and even healthy helps build perspective that such events can create as much opportunity as they do concern.

2) Recessions and corrections are points in time, while wealth-creating bull markets happen over time

Markets have been incredible creators of wealth over time. Below we demonstrate not just the frequency of bull versus bear markets, but the disproportionate outcomes skewed towards the positive. The total return of bull markets over time has been nearly 8x the drawdown of bear markets and have persisted over 5x as long.

It is also worth noting that these returns happened over a period in which the U.S. was engaged in four wars (Korean, Vietnam, Persian Gulf and the War on Terror), a Presidential assassination, Civil Rights riots, stagflation, higher interest rates, lower interest rates, multiple recessions, etc. The resilience of wealth creation builds context for the period in which we live now and how it may feel volatile or unprecedented. It is not unprecedented, and this too shall pass.

3) Market Timing– Getting it right is hard and getting it wrong is costly

Market timing requires three things to get it right: correctly timing the sell, doing it in a large enough size that it matters and correctly timing the buy on the way back in. Timing “buys and sells” is difficult because it involves having the fact pattern right and the appropriate market reaction to execute it consistently. As an analogue to why this is so hard, let’s pretend it is 2019. You are told that next year the U.S. economy will go into a recession, unemployment will be high, large sections of the country will be shut down and over 300 thousand people in the U.S. will die from a pandemic not seen in modern times. Not only is that set of facts nearly unknowable ahead of time, but even fewer would look at that information and predict the market would end the year up 19 percent.

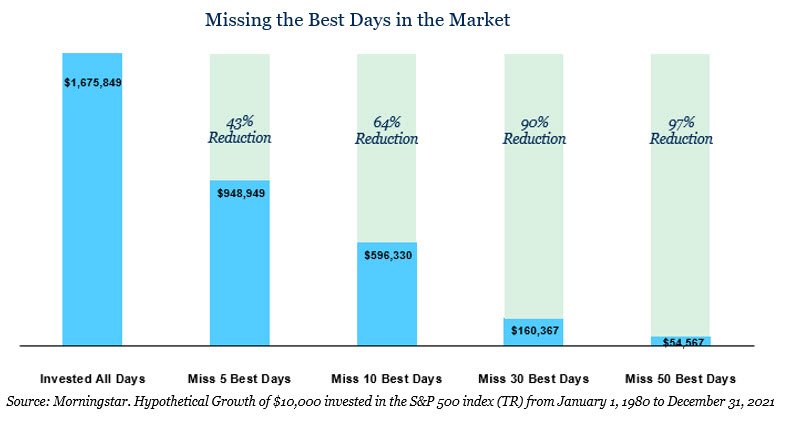

Moreover, the cost of market timing can be high when you get it wrong. As shown below, missing just a few of the best trading days can have a material impact on the overall return of the portfolio. Additionally, the vast majority of the best days in the market happen during market pullbacks. At the times it is most tempting to make a move, it may also be the most dangerous time to do it.

4) Recession obsession: don’t focus too much on the wrong thing

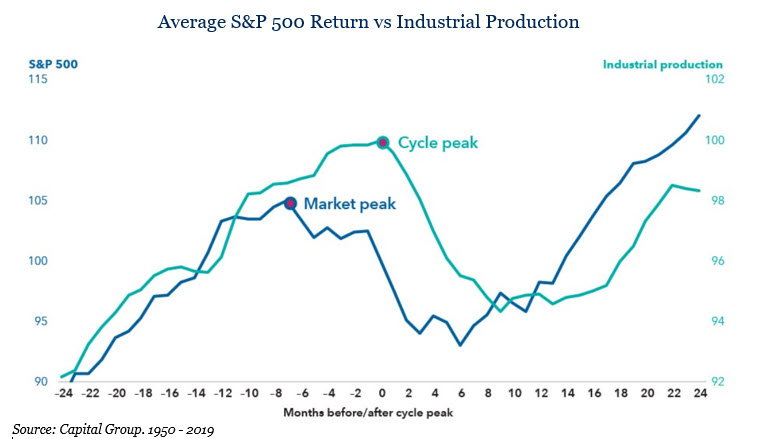

In periods of market volatility, investors’ gazes often turn to judging whether a recession will occur. Recession-seeking may be a red herring when it comes to investing. Markets attempt to look forward to predict the future while economic data is inherently backward looking. On average since 1950, markets have peaked seven months prior to an economic peak and bottomed three months before the economy began growing again. While a recession may help provide context around the potential depth or length of a pullback, it may not be the most helpful focus point for market outcomes.

5) Investing on emotion may feel right at the time, but is less likely to be a profitable approach

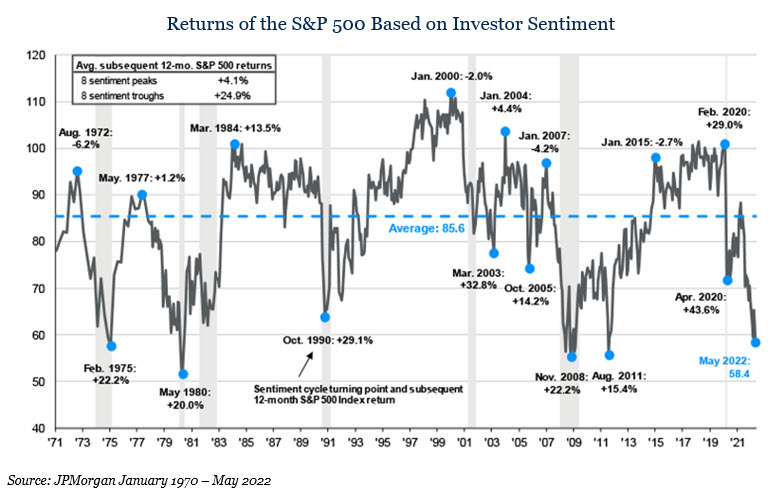

As humans we are hardwired to act, especially when we feel uncomfortable. After all, both fight and flight are responses. Thus, we find it hard to “do nothing.” One of our best proxies for feelings in the market is consumer sentiment. When sentiment is low, investors are pessimistic and the innate feeling to act is high. If sentiment is high, investors are optimistic about the future. However, if we look back at how profitable feelings are, we quickly learn that following our gut may not be the most beneficial approach. In fact, investing when things feel the worst on average has been 6x more successful than the opposite.

In times of plenty, investors often lose sight of basic building blocks of well-allocated portfolios. Fear of missing out when markets run up is a powerful motivator. We believe the following are elements of a more optimal approach for long-term success:

Stay Diversified – Diversification is an admittance of not knowing what the future holds. It also helps avoid acting in absolutes like “value will never come back” or “fixed income is dead.” The discipline of diversification often leads to a more robust approach that can help weather the inevitable storm markets create.

Stick to the Plan –

- If you don’t have a plan, get one (or contact us)

- Conceive your plan with realistic expectations on risk you can handle and returns you can achieve.

- When you have a plan, do not change it in the middle of the game. Have faith in the process and recognize the plan was built knowing recessions and bear markets would happen.

Long-Term is Where the Real Money is Made – This comment cuts at the heart of many truths in investing. Compounding over the long-term may be the 8th wonder of the world. Short-term expectations often lead to ‘flavor of the day’ investing, which rarely stands the test of time. No strategy works all the time, especially when passing judgment in a short window of time. Stay long-term and let the markets work for you, rather than you working against them.

For more information, please contact any of the professionals at Fiducient Advisors.

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses.

The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.