Key Observations

- Financial market returns year-to-date coincide closely with the premise of an expanding global economic recovery. Economic momentum and a robust earnings backdrop have fostered uniformly positive global equity returns while this same strength has been the impetus for elevated interest rates, hampering fixed income returns.

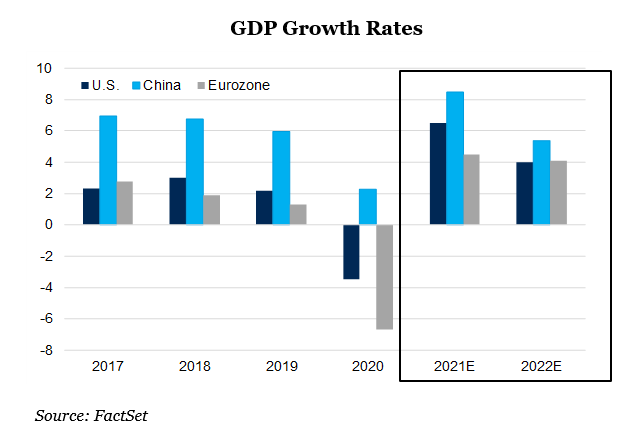

- Our baseline expectation anticipates that the continuation of the economic revival is well underway but its relative strength may be shifting overseas, particularly to the Eurozone, where amplifying vaccination efforts and the prospects for additional stimulus reign.

- Our case for thoughtful risk-taking remains intact. While the historically sharp and compressed pace of the recovery has spawned exceptionally strong returns across many segments of the capital markets and elevated valuations, the economic expansion should continue apace, fueled by still highly accommodative stimulus, reopening impetus and broader vaccination.

Financial Market Conditions

Economic Growth

Forecasts for global economic growth in 2021 and 2022 remain robust with the World Bank projecting a 5.6 percent growth rate for 2021 and a 4.3 percent rate in 2022. If achieved, this recovery pace would be the most rapid recovery from crisis in some 80 years and provides a full reckoning of the extraordinary levels of stimulus applied to the recovery and of the herculean efforts to develop and distribute vaccines.

While the case for further global economic growth remains compelling, we are mindful that near-term base effect comparisons and a bifurcated pattern of growth may be masking some complexities of the recovery. It is anticipated that a year-end 2021 global output will still be about 2 percent below its pre-pandemic level with many countries not fully recovering output until 2023.

Monetary Policy

While a narrative centering on the potential for heightened inflation has taken hold among investors, the Fed left the existing (and highly accommodative) rate policy and asset purchasing program unchanged at its June meeting. Of note, 13 of the 18 governors now anticipate at least one rate hike being necessary by the end of 2023. Monetary policy elsewhere around the world, on balance, remains stimulative as authorities seek to strike a balance between fostering economic repairs and their respective policy objectives.

Fiscal Policy

Governments across the globe unleashed unprecedented amounts of fiscal stimulus in the immediate aftermath of the pandemic’s onset and measures of additional potential support persist. President Biden’s late May announcement outlining upwards of $6 trillion of supplemental spending serves as the readiest evidence of this pledge. However, we expect the global fiscal response, considered collectively, has likely peaked and that further efforts to initiate stimulus via these channels may prove to be less impactful. In our view, fiscal largesse retains the capacity to vitalize economic activity in the near-term, but investors should be alert to the possibility that the longer-term impacts of wide scale spending can serve as a headwind to economic growth.

Inflation

Perhaps no topic has garnered a higher level of financial press and investor attention than inflation over the last few months. A global economy under rapid repair resulted in supply chain disruptions and notably higher input prices, fueling speculation that inflation may be on an accelerated trajectory to outpace the Fed’s longstanding 2 percent target. However, more recent moderations in, for example, raw material prices suggest some of these pressures are beginning to alleviate as organizations undertake the steps necessary to recalibrate their operations. We accept the Fed’s premise that inflation is likely to run at a meaningfully elevated level in the near term before ultimately settling at a higher than pre-pandemic level, but at a rate that should not threaten the global recovery. Please click here to watch our recent question and answer session with PIMCO’s Tiffany Wilding for more perspective on the inflation front.

Currency

The Fed’s recent more hawkish tone, while very preliminary and measured, has resulted in a bout of U.S. dollar strength despite the greenback’s somewhat lofty valuation and the geographically broadening economic recovery on display. Otherwise, the dollar was trending weaker for much of the second quarter. Absent a material flight to quality/risk-off market event, we expect the dollar to be range-bound, taking its directional cues from developments on the global economic front and the policy responses devised by authorities to mitigate, what are certain to be, differentiated paths to recovery.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.