Filter out the noise and stay the course

Key Observations

• Broad asset classes rose higher off 2022 lows on cooling pricing pressures and the possibility of a Fed pause

• Equities abroad outperformed amid a declining U.S. dollar and higher than expected growth

• The U.S. debt ceiling has sparked conversation, however the need for a resolution will likely abate an insolvency crisis

Market Recap

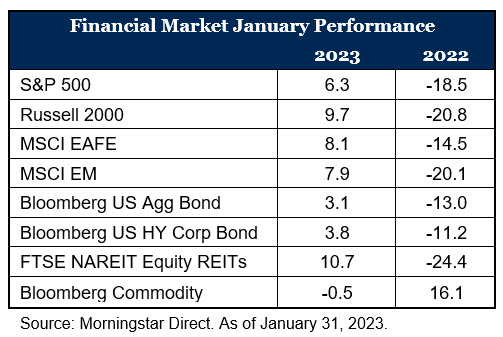

Broad asset classes kicked off the new year higher after a not-so-jolly December. Sentiment turned decidedly positive based on slowing wage and job growth and cooling price pressures. These trends provided optimism for a less hawkish Fed pushing investor expectations from a 0.50% Fed move in February to a 0.25% as of January 31, 2023.1 Optimism was tempered as investors assess how the economy is weathering higher interest rates, with retail sales and producer pricing showing signs of slowing in the U.S. economy.

While these appear to be signs the Fed’s fight against inflation may be working, investors continue to weigh the economic cost and viability of a “soft landing” scenario.

Fixed income markets saw a bright start to the year after a muted December, with the 10-year U.S. Treasury yield dropping 35 basis points (bps) as investor demand increased largely on more attractive yields.2 The yield curve remained inverted with the 10-year Treasury 68 bps below the two year.2 Lower quality, high yield bonds outperformed investment grade as sentiment turned positive.

The S&P 500 returned 6.3% with domestic winners coming from small caps (+9.7%) and growth-oriented securities (+8.4%3). Higher interest rates in 2022 had a material influence on high-growth businesses like the technology sector which lagged many other parts of the market. A more moderate Fed helped fuel their bounce back and the technology-heavy NASDAQ marked its best start to the year since 2001 up 10.7%.2 Non-U.S. equities rose in the month and widely outpaced their domestic counterparts with tailwinds from a declining U.S. dollar, higher than expected growth in Europe and positive sentiment around China easing restrictions on zero-COVID policies.

Diversifying and inflation sensitive areas of the market such as REITs and commodities were bifurcated in performance, with REITs rallying from 2022 lows and a warmer winter in Europe dragging energy prices and commodities slightly lower.

The Debt Ceiling Distraction

Historically this budgeting statute has been more procedural than material. However, recent rising debt-to-GDP levels and partisan politics turned procedure into brinksmanship; and similar standoffs in 2011 and 2013 resulted in market volatility. In all, we believe manufactured crises like these are more noise than signal when it comes to a sound investment strategy. In our recent blog post, The Debt Ceiling Distraction, we unpack why we believe this may be an issue that grows over time, but ultimately is resolved without creating lasting systematic issues.

Outlook

Fresh off our 2023 Outlook – Goodbye TINA research paper, we believe elevated volatility, moderating inflation and markets finding a bottom following the 2022 route will be key factors to position portfolios in 2023. Headline CPI data in December gave us a fresh look into moderating inflation. While year-over-year inflation grew at 6.5%, annualized inflation over the last six months was just 0.34% providing optimism for a soft landing and the Fed moderating their hawkish stance.4 It is perhaps too early to claim victory on price stability, however, these are steps in the right direction. As for what inflation and higher rates are doing to company earnings, those impacts are just coming to the surface with the majority of fourth quarter 2022 earnings data being released in February. The barrage of layoff headlines in sectors most impacted in the recent pullback may be an early signal of what is to come from the final quarter of 2022. This incremental information continues to support our positioning of building greater resiliency in portfolios while positioning for upside potential.

For more information, please contact any of the professionals at Fiducient Advisors.

1CME Group Feb 1 Fed Target Probabilities, January 31, 2023

2Morningstar: NASDAQ 100 as of January 31, 2023.

3Morningstar: Russell 3000 Growth as of January 31, 2023.

4Bureau of Labor Statistics as of December 31, 2023.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.