A look back on the Qualified Default Investment Alternative (QDIA) landscape in 2025

Key Observations

• Target date portfolios continue to be a cornerstone of defined contribution (“DC”) plans

• Managed account uptake has slowed, but evolution in the space is accelerating

• Consideration of alternatives in DC plans – target date and managed accounts could be the low-hanging fruit

The landscape for QDIAs has continued to evolve in recent years and we expect this trend to continue given the important role these options play in defined contribution plans. From the early days when static balanced funds and stable value solutions were the most widely implemented options, to today’s environment where target date and managed account solutions are seeking ways to incorporate private markets and income solutions for participants, target date solutions continue to be preferred by an overwhelming majority of Plan Sponsors. They serve as both the most common default offering and the largest recipient of participant cash flows in investment menus, now estimated to account for over $5 trillion in assets1. Target date funds remain the most common QDIA solution for Plan Sponsors, maintaining their popularity over time. Despite this consistency, the target date fund landscape is anything but stagnant, with ongoing developments shaping the space.

Persistent Trends

Target date trends noted in previous versions of this report persisted throughout 2025. Passive target date solutions attracted the majority of asset flows, Collective Investment Trust (CIT) vehicles continued to gain popularity and glide paths progressively increased their equity exposure. The following observations highlight the impact of these trends:

- Passive solutions generally offer lower expenses than hybrid or fully active counterparts, but it is important to note there is no truly passive option as active decisions must be made for the determination of strategic asset allocation, building blocks and setting the objectives.

- Collective Investment Trust (CIT) vehicles continue to attract interest within the institutional investing industry, in part due to their potential for greater fee flexibility along with lower overall fees. In addition, improved transparency and reporting has occurred in recent years for these vehicles, reducing Plan Sponsor hesitancy. CIT vehicles have captured the majority of target date flows since 2020 and are now estimated to make up more than 50% of all target date assets2.

- Strategic Glide Paths for target date funds are increasingly emphasizing equity allocations. This trend is supported by lower capital market expectations, participant demographic characteristics and evidence indicating that individuals invested in target date funds exhibit lower trading frequency and do not engage in market timing.In fact, Vanguard notes in a 2026 report that “Pure target-date fund (TDF) investors are much less likely to trade – typically four to five times less likely than other participants, a rate considerably lower than that of other investors…The reduced trading among pure TDF investors suggest a focus on long-term growth and stability and less reactive behavior during periods of market fluctuations”3.

Managed Accounts

Managed accounts have seen tremendous increase in uptake in recent years, with approximately 45% of Plan Sponsors offering this solution, up from 30% at the end of 20173. At the same time, participant utilization remains low and the rate at which new Plan Sponsors adopt the solution appears to have slowed. While off-the-shelf providers have long touted the benefits of managed accounts above standardized asset allocation products, there is an increased focus on participant behaviors as a measure of success for these solutions. Morningstar’s recent research report indicates that better outcomes for participants stem from both savings and asset allocation, with higher contribution rates being the main factor.

As consultants and Plan Sponsors continue to navigate the managed accounts space and the potential benefits to participants, a new version of managed accounts has grown in popularity in the form of Advisor Managed Accounts (AMAs). AMA solutions offer similar advantages to standard managed account products, but they also include the expertise of a designated advisor or consultant who contributes their asset allocation and fund selection skills. As Plan Sponsors dig into the philosophy and process behind off-the-shelf managed account solutions, while also seeking to provide solutions that are customized to their participant demographics, AMAs are becoming a more appealing option.

Alternatives in Defined Contribution Plans

In 2025, a significant focus for defined contribution plans was how they reacted to the executive order and government guidelines from Washington, which aimed to expand access to private markets to a broader class of investors through these plans. In response to these guidelines, the asset management community promptly announced new plan solutions that incorporated private market alternatives. Most of these offerings are either built on the chassis of a target date solution or provided as a building block for managed account utilization. Despite guidance on the inclusion of these types of investments, adoption by Plan Sponsors remains extremely low given the infancy stage of these products and the myriad of other factors Plan Sponsors will need to consider. It is estimated that within the overall target date market, only $115 billion is allocated to solutions with private equity and/or private real estate exposure4.

Plan Sponsors will have a number of considerations to navigate with incorporation of these types of securities, including, but not limited to:

- Liquidity

- Opaque valuation methods

- Portability (for participants and Plan Sponsors)

- Fees and fee complexity

- Limited track records

- Participant understanding

- Litigation and regulatory uncertainty

- Operational complexity and recordkeeper availability

- Governance and process

While the executive order created increased buzz, it is important to note there are several target date solutions that have already incorporated private market securities. Private real estate has been the most commonly used alternative historically, though the recent trend is for greater inclusion of different alternatives, including private credit and private equity mandates. Private markets may offer potential diversification and return enhancements, but they also introduce meaningful fiduciary complexity. Key areas demanding caution include liquidity management, valuation transparency, fee structures, portability challenges and limited DC-specific track records. For many committees, the central question is not simply whether private assets belong in retirement plans, but whether current structures allow sponsors to uphold longstanding fiduciary principles: clarity, fairness, simplicity and prudent oversight.

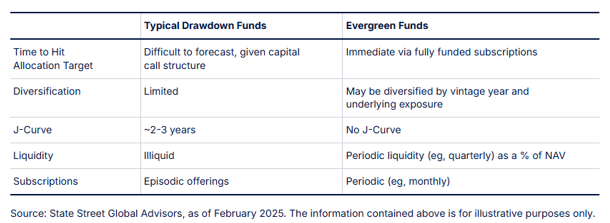

Despite these considerations, private investments now make up a greater portion of the investable universe and have shown additive diversification benefits alongside public securities for a wide array of other institutional investors, suggesting their inclusion in DC plans might offer a similar benefit. Recent developments in structure have also been a tailwind to consideration as more evergreen type vehicles provide liquidity more aligned with retirement plans needs and are gaining popularity. This structure seeks to mitigate many of the potential issues stated above and serves as a better building block for managed solutions because of its semi-liquid and perpetual nature.

Accumulation, Decumulation or Both?

While Plan Sponsors and advisors have predominately focused on the accumulation phase of retirement planning, greater attention is now placed on the decumulation phase. Americans today have greater reliance on their defined contribution assets as the primary tool to fund their retirement given that corporate pension plans are less common and there is growing uncertainty around Social Security benefits. As a result, the industry has launched solutions looking to address retirement spending via the decumulation of defined contribution assets. Many of these new solutions are intended to be incorporated into target date funds or managed accounts to further the efficacy of these strategies. Additionally, many of these solutions have integrated insurance components including SPIAs, QLACs, GMWBs and other structures to create income streams backed by an insurance guarantee in hopes to replicate the experience provided by pension plans of the past. While still new, Plan Sponsors have been keen to monitor these developments. However, there are many unique considerations to contemplate before selecting an income solution for participants. These include:

- A Lifetime Income option could be a matter of (settlor) plan design or a (fiduciary) administrative/investment decision (or both).

- The marketplace of Lifetime Income options and providers is new and rapidly evolving. There is limited experience and track record for many options and providers.

- Evaluating the insurance aspects of certain Lifetime Income options is a new and unique undertaking for many plan fiduciaries.

- Similarly, implementing and communicating unique and potentially complex Lifetime Income options to participants raises new considerations and burdens for plan fiduciaries and third-party providers.

Continued Evolution in the QDIA Space

The developments in QDIA solutions in recent years highlight the broader evolution of investment options within the defined contribution space. While target date solutions seem to have cemented themselves as a cornerstone of plan menu design, developments such as vehicle structure, active/passive implementation, and increased equity glide paths continue to take shape., QDIA adoption, strong participant utilization, by participants, market appreciation, and strong market performance have made target date solutions an important component of the defined contribution marketplace. In addition to the developments cited, other trends also appear on the horizon for QDIA solutions, including personalization, advisor managed accounts and inclusion of private market alternatives.

In the nearly 20 years since the Pension Protection Act paved the way for adoption of QDIAs, they have grown to be one of the most impactful developments in the retirement industry. With ongoing evolution and further guidance from regulatory bodies, these investment solutions will continue to play a crucial role in helping participants achieve their financial goals and secure their financial future. By staying informed and making strategic decisions, Plan Sponsors can maximize the benefits of QDIA offerings. As Plan Sponsors and participants continue to navigate these changes, the importance of prudent evaluation and selection of QDIA and target date funds remains paramount. To better understand how these evolving QDIA trends may impact your plan, contact the professionals at Fiducient Advisors for a tailored discussion.

For additional insight into the regulatory environment influencing default investments, explore our analysis of the Department of Labor’s new investment selection proposal.

1Sway Research – Target Date

2Morningstar, 2025 Target-Date Fund Landscape, April 2025

3Vanguard, How America Saves 2026

4State Street Investment Management, Private Markets in Target Date Funds – Why Now?, March 7, 2025

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.