Strong Q1 earnings fuel global rally and reinforce the case for diversification

Key Observations

• Global equities rebounded sharply in April. Strong Q1 corporate earnings, led by mega-cap technology, restored investor confidence after a turbulent start to the year shaped by the conflict with Iran.

• Diversification beyond U.S. large cap continued to pay. Emerging markets, international developed equities and U.S. small cap all delivered strong returns.

• The Federal Reserve held its policy rate at 3.50% to 3.75% as it weighed inflation pressure from higher energy prices against a softening labor market. April marked Chair Powell’s final FOMC meeting in that role.

Market Recap

April delivered a sharp recovery for global markets. After a difficult start to 2026 marked by the escalation of the Iran conflict and broader concerns about growth and inflation, investor sentiment shifted during corporate earnings season. Strong results, particularly from large U.S. technology companies, sparked a rally that pushed equities higher.

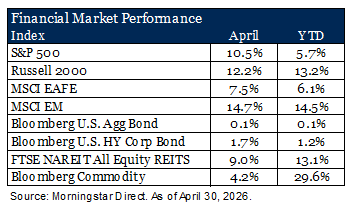

Large cap U.S. equities gained double digits, as the S&P 500 Index returned 10.5% for the month, supported by leadership from communication services, information technology and consumer discretionary. Positive earnings surprises from Alphabet, Amazon and Meta drove much of the upside. Smaller companies advanced even faster. The Russell 2000 Index gained 12.2% as easing recession concerns and improving earnings breadth across cyclicals supported a sharp rally. Information technology and industrials led the small-cap space, while energy and health care lagged. International equities also delivered strong returns. The MSCI EAFE Index rose 7.5%, with broad participation across Europe and Japan. Information technology, industrials and financials led the regional advance, while a weaker U.S. dollar amplified returns for U.S. investors and added more than 200 basis points to the index’s monthly gain. Emerging markets posted the strongest equity performance of the month. The MSCI EM Index climbed 14.7%, propelled by a 32.2% surge in the Information Technology sector as semiconductor and AI infrastructure demand continued to reaccelerate. Korea, Taiwan and India led individual markets, and the asset class is now up nearly 47% over the past year.

Fixed income produced more modest gains. The Bloomberg U.S. Aggregate Bond Index returned 0.1% as Treasury yields traded in a tight range but ultimately ended the month higher. The Federal Reserve held its policy rate at 3.50% to 3.75% at its April meeting, citing the need to assess the inflationary effects of higher energy prices alongside a cooling labor market. It was the third consecutive pause and Chair Powell’s final meeting in that role. Credit markets fared better. Spreads tightened on the back of the equity rally and stronger earnings, helping the Bloomberg U.S. Corporate High Yield Index advance 1.7%.

Real assets rounded out a constructive month. The FTSE NAREIT All Equity REITs Index gained 9.0%, with broad-based participation across property types. Office REITs jumped 13.6% on signs of stabilization in major metropolitan markets, and lodging, data centers and self-storage all rallied alongside improving fundamentals. Commodities advanced more modestly. The Bloomberg Commodity Index rose 4.2% as oil prices modestly consolidated after their early-year surge tied to the Iran conflict. Industrial metals and agriculture contributed positive returns, and gold finished roughly flat near record levels.

Strength and Resiliency in U.S. Equity Earnings

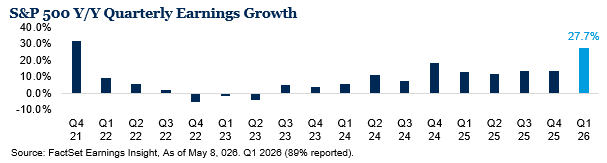

Q1 2026 earnings season has been the strongest in nearly five years. Blended year-over-year EPS growth for the S&P 500 is tracking at 27.7% (with 89% reporting), the highest since Q4 2021 and more than double the 13.1% expectation at quarter end. If realized, it would mark the index’s sixth consecutive quarter of double-digit growth and its strongest quarter since Q4 2021.1

Mega-cap technology continues to disproportionately lift headline earnings. Strong results from Alphabet, Amazon, Meta and Microsoft drove most of the upside, lifting the “Magnificent 7” earnings growth to 61% versus 16% for the rest of the index.2 AI capital spending continues to set the pace. Hyperscaler capex commitments for 2026 climbed to roughly $751 billion, an 83% increase from 2025 spending.3 That investment is feeding through to revenue and earnings momentum at chipmakers, infrastructure providers and select industrials, while at the same time raising legitimate questions about returns on capital. Another important note this quarter is the share of “other income” contributing to the growth. Nearly 60% of net income for Google and Amazon came from valuation increases to private company holdings such as Anthropic.3

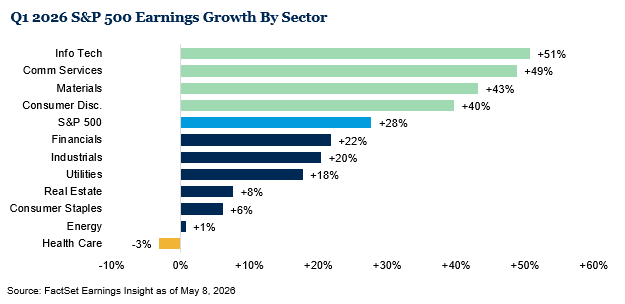

Looking deeper at specific sectors, seven of eleven S&P 500 sectors are reporting double-digit year-over-year earnings growth. Information technology (+51%), communication services (+49%), materials (+43%), and consumer discretionary lead the index. NVIDIA and Micron Technology were key drivers within information technology, benefiting from strong AI-related demand for semiconductors. Health care is the only sector showing year-over-year declines. Beneath the surface, results were broader than the headline numbers suggest. Industrials and Financials posted a solid quarter with positive guidance, and more broadly companies reported the lowest frequency of EPS misses in 25 years (excluding COVID).3

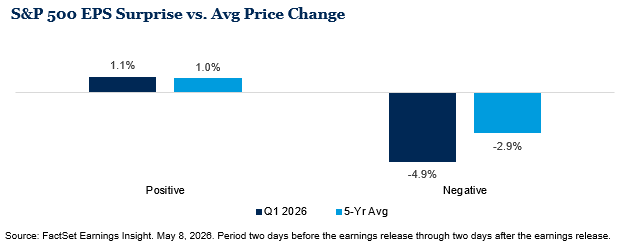

Equities responded constructively and the risk-on tone was visible across global markets. Beneath the surface, however, the reward for individual EPS beats has been unusually small. The median company beating consensus outperformed the index by just 20 basis points the day after reporting, one of the smallest readings on record.

On the other hand, companies with negative earnings surprises were disproportionately punished. That suggests good news was largely priced in. Capital spending also outpaced share repurchases by a wide margin, with capex up over 40% year-over-year in Q1 versus a 1% increase in buybacks, something that warrants monitoring.4

Strong earnings remain the primary support for current valuations. The S&P 500’s forward P/E of 21x sits above its five-year average of 19.9x and ten-year average of 18.9x, but the multiple is more digestible if 2026 earnings deliver the 21% growth analysts now expect.5 The path to that outcome requires margins to hold and AI capex to continue translating into revenue. There are risks to this, particularly around margin compression. Tariffs, energy costs and wage pressures could erode the profitability gains analysts are projecting. And market concentration combined with elevated valuations leaves less margin for disappointment.

Outlook

April reminded investors how quickly sentiment can shift when fundamentals reassert themselves. After a turbulent start to 2026, strong corporate earnings and easing tensions in the Middle East provided a powerful counterweight to macro headwinds earlier in the year and lifted nearly every major asset class. The themes from our 2026 Outlook continue to play out. Diversifying away from U.S. large cap has been beneficial year to date, with small caps, international developed equities and emerging markets all leading. AI-related capital spending is broadening into more parts of the economy, and companies are delivering solid earnings growth.

We remain mindful of the cross-currents. Valuations are stretched, market concentration is elevated, sentiment improved meaningfully and the macro backdrop remains uncertain with the Iran conflict, tariff implementation and a Federal Reserve transition all in motion. Strong fundamentals are an important tailwind, but they argue for thoughtful diversification rather than concentrated bets. We continue to favor portfolios that are positioned to participate in the broadening of returns while protecting against the risks that elevated valuations introduce.

1FactSet Earnings Insight as of May 8, 2026

2FactSet Earnings Insight, May 1, 2026.

3Goldman Sachs U.S. Weekly Kickstart, May 1, 2026. Based on 5 largest public hyperscalers (AMZN, GOOGL, META, MSFT, ORCL)

4Goldman Sachs U.S. Weekly Kickstart, May 1, 2026.

5FactSet Earnings Insight. May 8, 2026.

Disclosures & Definitions

Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and do not reflect our fees or expenses. Market returns shown in text are as of the publish date and source from Morningstar or FactSet unless otherwise listed.

- The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

- Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

- MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the U.S. and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

- MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country.

- Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

- Bloomberg U.S. Corporate High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

- FTSE NAREIT Equity REITs Index contains all Equity REITs not designed as Timber REITs or Infrastructure REITs.

- Bloomberg Commodity Index is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification.

Material Risks

- Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

- Cash may be subject to the loss of principal and over longer periods of time may lose purchasing power due to inflation.

- Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

- International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impacted by currency and/or country specific risks which may result in lower liquidity in some markets.

- Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

- Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class like leverage and/or industry, sector or geographical concentration. Declines in real estate value may take place for a number of reasons including, but are not limited to economic conditions, change in condition of the underlying property or defaults by the borrower.

- All investing involves risk including the potential loss of principal. Market volatility may significantly impact the value of your investments. Recent tariff announcements may add to this volatility, creating additional economic uncertainty and potentially affecting the value of certain investments. Tariffs can impact various sectors differently, leading to changes in market dynamics and investment performance. You should consider these factors when making investment decisions. We recommend consulting with a qualified financial adviser to understand how these risks may affect your portfolio and to develop a strategy that aligns with your financial goals and risk tolerance.

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.