We’re living in one of the most unusual market environments in decades. Valuations are elevated, AI is reshaping everything, the Fed has been accommodating and geopolitical tensions are rising, fast! In times like these, wealthy investors may see opportunity but also heightened risk. Throughout my career in advising affluent families, nonprofits and other investors, I’ve seen patterns – both good and bad – that repeat themselves, as well as lessons learned.

Below are 10 mistakes wealthy investors should avoid this year, along with practical steps to stay on course.

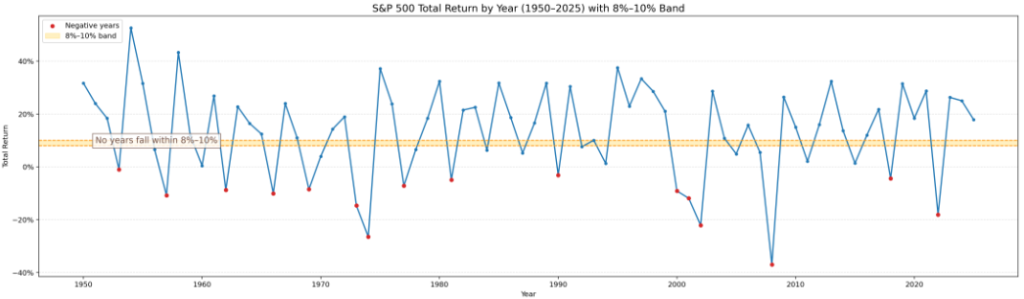

1. Expecting Market Returns to Be “Average”

Most investors think of the S&P 500 averaging roughly 8–10% annually over long stretches. Reality shows the index rarely lands in that range in any given year. As illustrated below, returns for the index didn’t fall into that range even once over the past 75 years. Typically returns are meaningfully higher or lower, sometimes dramatically.

Distribution of S&P 500 Annual Returns Over 75 Years

Source: Slickcharts

Investor takeaway: Don’t anchor on averages. Have a mindset that stock returns vary significantly, then think of that volatility as the “toll” for higher long-term performance.

2. Spending Like the Bull Market Will Last Forever

Strong markets create a powerful illusion: “My portfolio is growing… I must be fine.” But rapid spending growth and excessive leverage often go unnoticed until markets decline.

Two mistakes investors are prone to make in good times:

- Spending well above sustainable levels

- Carrying unnecessary debt

Upward markets can mask issues – downturns expose them quickly.

Investor takeaway: If your lifestyle depends on strong markets, your financial plan lacks durability.

3. Spending Too Little

On the flip side, one of the most common, but least discussed, mistakes among wealthy investors is optimizing portfolios while deferring life. As Bill Perkins notes in Die With Zero, “your life energy is limited.” For some, the real risk isn’t outliving your assets; it’s postponing meaningful experiences until health, time or family dynamics make them impossible, leaving behind a strong balance sheet but an under-lived life.

Fear of running out keeps some wealthy investors from enjoying experiences for themselves and their families.

Three steps can help you plan with confidence:

- Estimate your likely annual withdrawals. This seems obvious, but you’d be surprised how often very wealthy individuals fail to create even a high-level budget. As a result, they never become truly comfortable with their spending because they haven’t done the math.

- Ensure your asset allocation aligns with the required return.

- Run Monte Carlo simulations to assess long-term sustainability.

My colleagues in our Wealth Office™ can help add clarity and discipline.

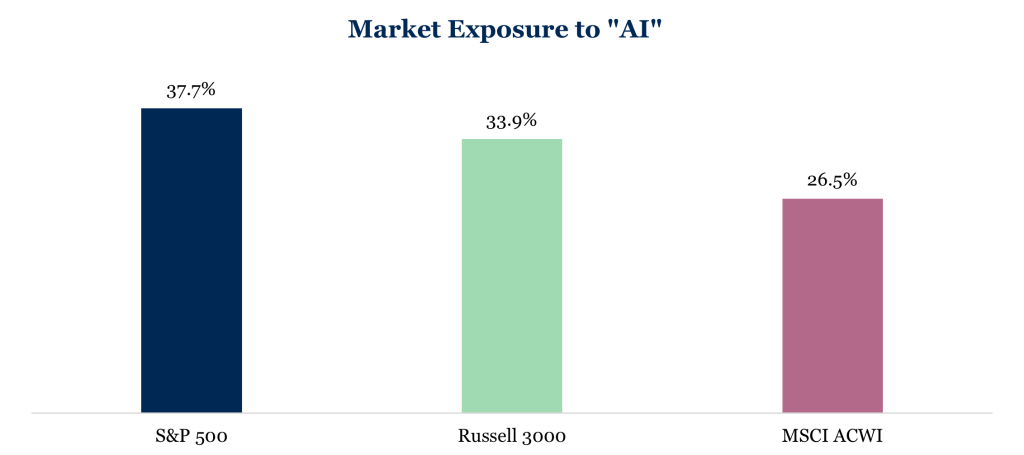

4. Thinking You’re Not Exposed to AI

Some investors tell me, “I’m not chasing AI stocks.” But if you own broad index funds, you own AI through hyperscalers like Microsoft, Alphabet, Amazon and through companies powering AI infrastructure such as semiconductors, data centers and energy providers.

AI has been a major driver of market returns. But valuations are stretched, and history shows that disruptive technologies produce big winners and many losers.

Sources: BlackRock, Morningstar, Fiducient Advisors. As of November 30, 2025. Exposure to “AI” based on the common holdings compared to the following indexes: Morningstar Global Artificial Intelligence Select Index; NYSE Semiconductor Index; S&P Data Center, Tower REIT and Communications Equipment Index; Morningstar Global Digital Infrastructure & Connectivity Index.

Investor takeaway: Understand your exposure to AI. Being overexposed introduces risk; having zero exposure misses opportunity.

Check out our 2026 Outlook on AIO and more here.

5. Failing to Broadly Diversify

With lofty valuations, rising deficits and growing geopolitical uncertainty, diversification matters now more than ever.

History provides a powerful reminder. In 1989, Japanese equities represented roughly 50% of global stock market capitalization, and I think you’d be surprised to learn (or remember) that eight of the world’s ten largest companies were Japanese! The momentum appeared unstoppable. What followed were decades of stagnation. And today? Japan comprises only about 5% of global equity market capitalization.

The Need to Diversify: Shifting Global Landscapes

Sources: Credit Suisse Global Investment Returns, MSCI ACWI / ACWI IMI, Visual Capitalist, LPL Research

With the U.S. today accounting for nearly two-thirds of global market capitalization, the lesson is not that the U.S. will necessarily repeat Japan’s experience. Rather, it is that market leadership changes, often in ways few investors anticipate. Periods of extreme dominance, no matter how compelling the narrative, have historically proven temporary.

Investor takeaway: Concentration builds wealth; diversification preserves it. Thoughtful diversification can include not only diversifying equity holdings but adding bonds, alternatives and more.

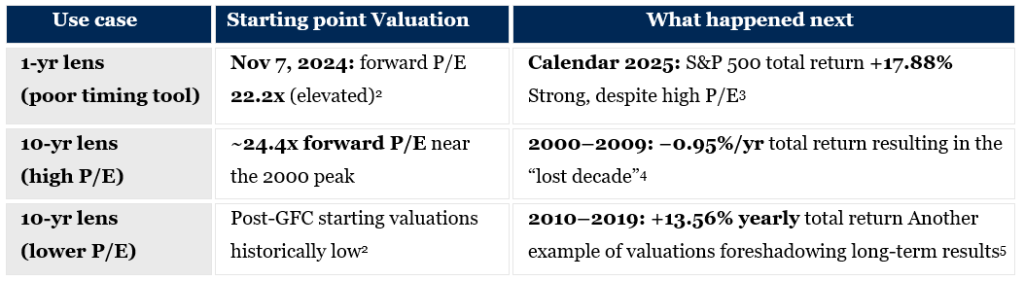

6. Assuming High Valuations Mean a Crash Is Imminent

Yes, valuations are elevated with the S&P 500 trading at a forward P/E of approximately 22 compared to the 25-year average of 16.7.1

But here’s an important insight: Valuations are poor predictors of performance over the short-term.

High valuations can stay high or move higher. Low valuations can remain depressed for extended periods. The following provides real world examples of why valuations are much more helpful over longer periods.

Sources FactSet, dimensional.com, sparkwealthadvisors.com, ishares.com, slickcharts.com

Investor takeaway: Use valuations to set reasonable long-term expectations, not to time markets.

7. Not Being Liquid… Enough

Many wealthy investors allocate meaningfully to private equity, venture capital, private credit and real assets. These can be powerful long term growth engines – but also come with capital calls, potentially arriving at precisely the wrong moment.

Consider the possibility of a 25% public market decline, followed by ongoing capital calls from private investments. Does your portfolio have ample liquidity to fund obligations without forcing sales at depressed prices?

And remember that liquidity shortfalls rarely appear in isolation. They tend to surface when markets are dislocated, correlations rise, and flexibility matters most. At those moments, even well-constructed portfolios can face challenges if liquidity was underestimated.

Our Fiducient Private Markets team regularly helps investors model commitment pacing, expected drawdowns and liquidity buffers; stress testing portfolios in advance so decisions during periods of market strain are deliberate, not reactive.

Investor takeaway: Illiquidity can enhance long term returns – but only when it is intentionally sized and thoughtfully managed.

8. Not Having a Pre‑Defined “Plan B” for Spending

Even very wealthy families may need, or choose, to adjust spending during severe market downturns. The difference between confidence and stress is rarely net worth – it’s whether those adjustments have been thoughtfully considered in advance.

A well designed Plan B isn’t necessarily about sacrifice. It’s about optionality and knowing which expenses are flexible, which are essential, and which can be deferred if conditions warrant.

Your Plan B might include:

• Deferring major purchases or capital intensive projects

• Temporarily scaling back luxury travel or discretionary experiences

• Reducing carrying costs by selling one of several homes

• Modifying or pausing financial support for adult children

I believe that financial strength comes not just from your resources, but from your readiness.

Investor takeaway: Define spending priorities, and tradeoffs, before markets force the exercise.

9. Failing to Control What You Can Control

Markets are unpredictable; costs and taxes are not. Yet many investors overlook the elements fully within their control – fees, and even more important, tax drag.

Unfortunately, inefficiencies in these areas compound just as reliably as investment gains. Fund and advisory fees, transaction costs, and interest expense quietly erode returns, raising an important question: do you have a clear understanding of the true, all in cost of your portfolio? On the tax front, unnecessary realized gains, poor asset location, and suboptimal loss harvesting can do even more damage. The result is a widening gap between market returns and what investors actually keep.

It is essential to incorporate asset location analysis (which accounts, which assets), capital gain budgeting, loss harvesting practices and disciplined cost controls into your portfolio construction and ongoing management. The objective isn’t to minimize costs at all costs; it’s to ensure that every dollar paid (or surrendered in taxes) has a clear purpose and measurable value.

Investor takeaway: It’s not what you earn – it’s what you keep. Control fees, allocate deliberately and build portfolios to generate attractive after-tax returns.

10. Managing Your Wealth Without an Intentional Strategy

The final (and often most costly) mistake is letting wealth drift without intentional direction. Business ventures, careers, family, health and more all compete for your attention. Decisions get made incrementally, portfolios quietly accrete positions, and assumptions go unexamined. What began as a thoughtful approach can slowly turn into a set of disconnected choices.

But strong outcomes rarely happen by accident. They come from clarity of priorities, disciplined decision-making and ongoing alignment between goals, spending, investments, risk, liquidity and tax considerations. Life does get busy… which is precisely why it’s essential to assemble the right team of advisors, including accountants, attorneys, investment advisors and others, who understand your objectives, challenge your assumptions and keep your plan on course when markets, or life itself, become uncomfortable or complex.

Investor takeaway: Great outcomes come from intention, alignment and accountability – not chance.

Final Thoughts

We live in exciting, and unusual, times. While every day brings us one step closer to the next bear market, it is also reasonable to believe this bull market may have room to run, supported by continued innovation, strong earnings and a more accommodative Federal Reserve.

The best approach is not prediction, but preparation. Be intentional in how you deploy capital across investments, spending, philanthropy and legacy goals. And as always, if you or someone you care about would benefit from thoughtful guidance, please reach out to me or any of us at Fiducient Advisors.

1Jan. 8, 2026: Trendonify and FactSet

2ishares.com

3dimensional.com

4sparkwealthadvisors.com

5slickcharts.com

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.