Reassessing the Evolving Market Landscape

Key Observations

• As outlined in our January 2022 Outlook – Navigating Moderation, we anticipated a challenging investment environment with heightened levels of volatility.

• The broad themes outlined at the beginning of the year – the evolving nature of the pandemic, central bankers’ balancing act and historically high inflation remain the prevailing themes. Along with the rising probability of recession, these themes will likely drive capital markets volatility throughout the second half of the year.

• As of June 13, 2022, the S&P 500 officially entered bear market territory, which is more than 20 percent below its all-time high set in January of 2022. In addition to a challenging global stock market rout, the 10-Year U.S. Treasury yield is up about 2 percent year-to-date (through June 14), making the first half of 2022 one the worst periods for the bond markets on record.

The State of the Broader Economy

With the economic fallout including the exacerbation of inflationary forces from the war in Ukraine, CPI at 40-year highs, a flattening yield curve bordering on inversion and a bear market in the S&P 500 index (as of June 13), recession expectations have been steadily rising during early 2022. Near-term economic and inflation data is likely to underwhelm if not disappoint, particularly on the heels of the strong economic advances in the aftermath of massive fiscal and monetary stimulus throughout the pandemic. In the current environment, even in the face of slowing economic growth and forward-looking growth expectations, the Fed has little wiggle room to focus on anything other than reining in inflation. Given the Fed’s failure to raise rates in 2021 in the face of what it called ‘transitory’ inflation at the time, it has no choice now but to play catch up to try to rein in inflation even if means causing a recession. As a result, global stock and bond markets have been grappling with increasing stagflation concerns, which have necessitated the broad repricing of financial assets that we have seen.

Our 2022 Themes – Revisited

1) From Pandemic to Endemic

Despite the general trend toward less virulent subsequent variants, we expect COVID-19 to continue to exacerbate supply chain bottlenecks particularly in China where a zero COVID-19 policy is still leading to unpredictable production stoppages and global economic growth headwinds. It is another factor leading to supply shortages and inflationary pressures.

Portfolio Impact

The Fed can only impact demand with monetary policy, but the supply bottlenecks are likely to continue for some time exacerbated by flair ups in COVID-19 infections. Expect supply chain bottlenecks to continue to weigh on production, economic growth and inflation forces.

2) Policy Maker Tightrope

Central bankers across the globe continue to implement an array of policy responses, crafted to answer to their own unique economic circumstances. While central banks in many advanced markets are raising rates to dampen inflation, conditions elsewhere have required more nuanced approaches – ranging from the European Central Banks’s near-term emphasis on quantitative tightening and higher rates to the People’s Bank of China’s efforts that lean into more stimulus to stabilize an economy recently maligned by widespread lockdowns in response to a COVID-19 outbreak.

Portfolio Impact

Exacerbated by disparate policy responses by central bankers across the globe, conditions remain unsettled with inflation and interest rates. We believe wise action remains to actively manage fixed income and mitigate overall portfolio duration through portfolio construction. Bolstered by a more favorable valuation profile, emerging market stocks may draw additional support from more stimulus in China and a marginally stabilizing global commodity complex. The Fed’s austerity campaign and a resilient U.S. Dollar could, however, serve as headwinds. However, the case for emerging market stocks persists as we mentioned in our January 2022 Outlook.

3) Inflation: Coming or Going?

Inflation continues to run at 40-year highs, which is untenable to the Fed. As shown by the Fed’s nearly unanimous approval of its 75 basis point hike on June 15, there will be a more accelerated and emphatic path to higher rates than expected as recently as last week or last month. Among Fed officials, the weighted-average expectation for the Fed Funds rate at year-end currently stands at 3.6 percent according to the CME FedWatch Tool as of June 17, 2022. One week ago on June 10, it stood at 3.3 percent and one month ago on May 17, it stood at 2.9 percent. The current Fed Funds Rate is 1.5-1.75 percent1.

Portfolio Impact

The path to a moderating inflation is likely to be choppy. Rising interest rates and a slowing economy could lead to waning inflationary pressures towards the end of 2022. However, as we outlined in our January 2022 Outlook, an allocation to real assets continues to be important to diversify and protect the portfolio from further rising inflation.

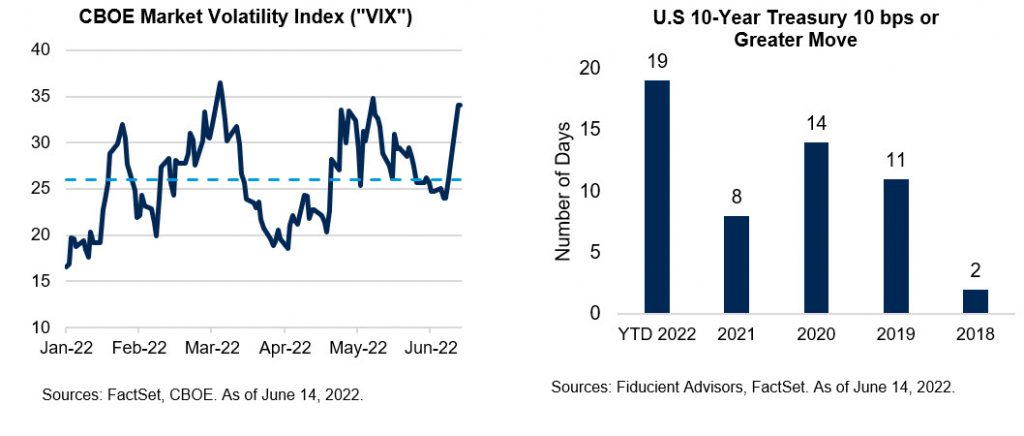

4) Volatility Ahead: Be comfortable with your risk posture

Equity markets no longer enjoy accommodative monetary policy and find their relative appeal more directly challenged by meaningfully higher bond yields. As investors find they can earn higher rates of return investing in bonds on a go forward basis, stocks reprice (down) until a new equilibrium is achieved. Interest rate volatility remains higher than normal as investors labor to gauge the Fed’s further policy intentions, which will be driven by inflation data. So far in 2022, the number of days where the U.S. Treasury has moved 10 basis points (0.10 percent) or more is well above the pace of previous years.

Portfolio Impact

We remain vigilant to the evolving conditions in markets. All things considered, we reaffirm the investment orientations that we shared with you earlier in the year; namely, our preference for a globally diversified equity profile, an inclination to diversify fixed income as to mitigate interest rate risks and our commitment to real asset exposure. In our opinion, this positioning should moderate the most stressful potential effects currently influencing markets.

Updated Market Forecasts & Portfolio Implications

Markets have been in a consolidating mode year-to-date as investors grapple with stubbornly high inflation, evolving Fed policy and the conflict in Ukraine. From the beginning of the year through June 16, domestic equities (S&P 500) have declined by 22.5 percent, while international equities (MSCI ACWI Ex USA) and U.S. bonds (Bloomberg US Aggregate Index) are down 18.34 percent and 11.5 percent, respectively2. Only commodities and related real assets have offered any protection to investors in 2022.

Our capital markets research team regularly surveys the investing landscape. When we see meaningful changes, we revise our forward-looking assumptions. We completed this exercise in early June for the period ending May 31. Our forward-looking return expectations for many asset classes increased due to this year’s wide scale repricing of markets as mentioned above.

Interestingly, the forecast revisions that were made did not generate meaningful changes to representative portfolios when run through our Frontier Engineer® portfolio construction framework. Markets retreated broadly across global fixed income and equity asset classes this year resulting in similar modifications in return expectations across broad and sub asset classes.

In summary, our best ideas portfolios remain in place as of this mid-year update. While markets during the first half of 2022 have been challenging, it is important to remember that they move based on changing expectations about the future. While painful in the short-term, the selloff has repriced many assets across fixed income and equity classes to more compelling valuations on a forward-looking basis. While it is foolhardy to predict market bottoms, it is important to note they have usually come with peaks in both pain and pessimism. It is unlikely to be different during this bear market. In full recognition of the rapidly evolving markets, we encourage engagement with your advisor to discuss the circumstances unique to your portfolios.

For more information, please contact any of the professionals at Fiducient Advisors.

1Federal Reserve. As of June 17, 2022

2Morningstar Direct. As of June 16, 2022

The information contained herein is confidential and the dissemination or distribution to any other person without the prior approval of Fiducient Advisors is strictly prohibited. Information has been obtained from sources believed to be reliable, though not independently verified. Any forecasts are hypothetical and represent future expectations and not actual return volatilities and correlations will differ from forecasts. This report does not represent a specific investment recommendation. The opinions and analysis expressed herein are based on Fiducient Advisor research and professional experience and are expressed as of the date of this report. Please consult with your advisor, attorney and accountant, as appropriate, regarding specific advice. Past performance does not indicate future performance and there is risk of loss.